微信扫一扫联系客服

微信扫描二维码

进入报告厅H5

关注报告厅公众号

Should central banks provide reserve accounts to everyone? A number of concrete proposals for central bank digital currency (CBDC) are now being discussed by policy makers as well as the general public. For example, the governor of the Swedish Riskbank has put the probability of issuing an "e-krona" within the next decade at greater than 50%.1 Moreover, in the June 2018 Vollgeld referendum, Swiss voters assessed (and, for now, turned down), a proposal to introduce non-interest paying CBDC. Along with this general interest, an emerging literature is weighing the pros and cons of CBDC.

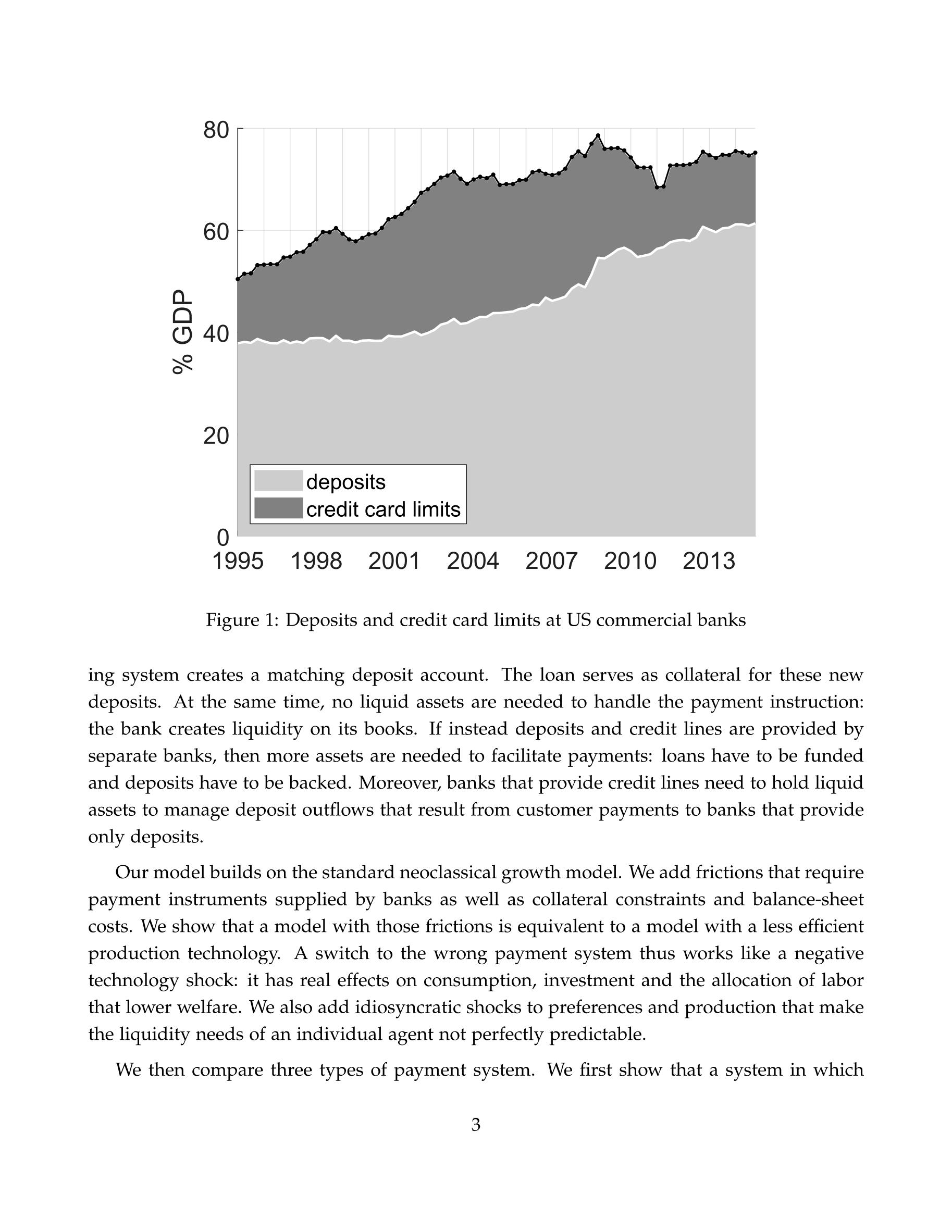

This paper is a theoretical study of the welfare effects of CBDC. Our approach is to view CBDC as a new product in the market for liquidity, broadly defined: CBDC competes not only with deposits, but also with credit lines offered by commercial banks for liquidity purposes. To illustrate the importance of credit lines for payments, Figure 1 plots deposits at all US commercial banks together with those banks’ outstanding credit card limits. Since credit card limits provide only a lower bound on credit lines used for payments – for example, the figure leaves out credit lines provided to asset management firms by their custodian banks – the message is that credit lines matter.

相关报告

银行业银行存款专题:揽储能力重要性凸显,关注长期竞争力差异-20210702-平安证券-28页

367

类型:行研

上传时间:2021-07

标签:银行、银行存款)

语言:中文

金额:5积分

纽约联储-谁付出代价?美国家庭信用透支上限和无银行存款(英)-2021.6

250

类型:专题

上传时间:2021-07

标签:美国、信用透支、银行存款)

语言:英文

金额:5积分

欧洲央行-不同目的地银行存款的不稳定:评估和政策影响(英)

119

类型:宏观

上传时间:2024-01

标签:银行存款)

语言:英文

金额:5积分

中央银行存款账户管理办法

90

类型:政策法规

上传时间:2023-07

标签:银行存款)

语言:中文

金额:5积分

银行行业专题研究:银行存款结构走弱导致存款成本刚性较强

53

类型:行研

上传时间:2024-03

标签:银行存款)

语言:中文

金额:5积分

积分充值

30积分

6.00元

90积分

18.00元

150+8积分

30.00元

340+20积分

68.00元

640+50积分

128.00元

990+70积分

198.00元

1640+140积分

328.00元

微信支付

余额支付

积分充值

应付金额:

0 元

请登录,再发表你的看法

登录/注册