微信扫一扫联系客服

微信扫描二维码

进入报告厅H5

关注报告厅公众号

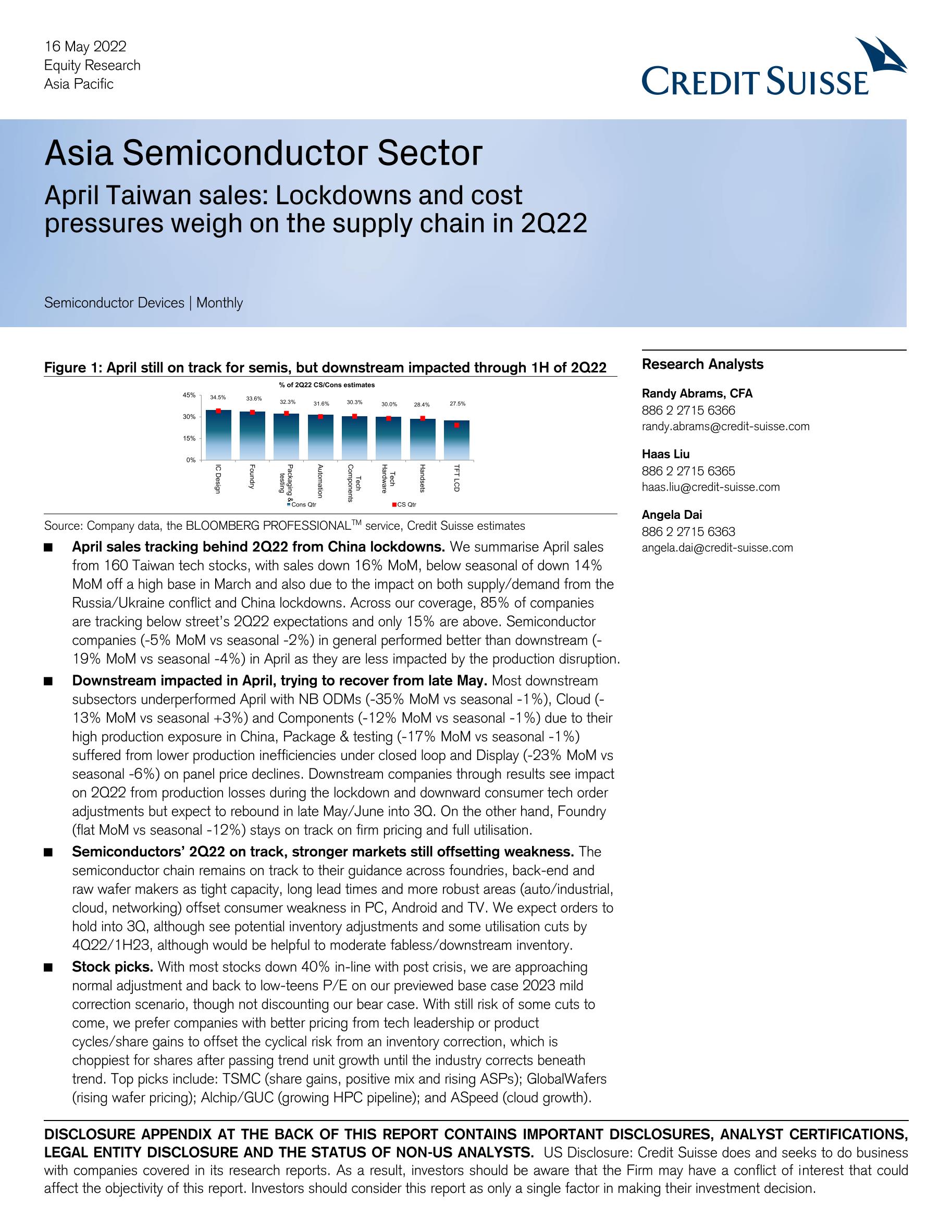

Source: Company data, the BLOOMBERG PROFESSIONALTM service, Credit Suisse estimates April sales tracking behind 2Q22 from China lockdowns. We summarise April sales from 160 Taiwan tech stocks, with sales down 16% MoM, below seasonal of down 14% MoM off a high base in March and also due to the impact on both supply/demand from the Russia/Ukraine conflict and China lockdowns. Across our coverage, 85% of companies are tracking below street’s 2Q22 expectations and only 15% are above. Semiconductor companies (-5% MoM vs seasonal -2%) in general performed better than downstream (19% MoM vs seasonal -4%) in April as they are less impacted by the production disruption.

Downstream impacted in April, trying to recover from late May. Most downstream subsectors underperformed April with NB ODMs (-35% MoM vs seasonal -1%), Cloud (13% MoM vs seasonal +3%) and Components (-12% MoM vs seasonal -1%) due to their high production exposure in China, Package & testing (-17% MoM vs seasonal -1%) suffered from lower production inefficiencies under closed loop and Display (-23% MoM vs seasonal -6%) on panel price declines. Downstream companies through results see impact on 2Q22 from production losses during the lockdown and downward consumer tech order adjustments but expect to rebound in late May/June into 3Q. On the other hand, Foundry (flat MoM vs seasonal -12%) stays on track on firm pricing and full utilisation.

Semiconductors’ 2Q22 on track, stronger markets still offsetting weakness. The semiconductor chain remains on track to their guidance across foundries, back-end and raw wafer makers as tight capacity, long lead times and more robust areas (auto/industrial, cloud, networking) offset consumer weakness in PC, Android and TV. We expect orders to hold into 3Q, although see potential inventory adjustments and some utilisation cuts by 4Q22/1H23, although would be helpful to moderate fabless/downstream inventory.

相关报告

高盛中国市场策略-2022市场展望:“不适”的上行空间;离岸市场重回超配

5353

类型:策略

上传时间:2021-11

标签:投行报告、中国、市场展望)

语言:中文

金额:5积分

德国智库9万字报告:与中国台湾打交道 (中英对照)

4210

类型:国际关系

上传时间:2022-09

标签:台湾地区、外交发展、两岸关系)

语言:中英

金额:7元

国际投行报告-全球芯片行业:芯片的冲突-台积电、三星和英特尔(英)

3973

类型:行研

上传时间:2022-06

标签:投行报告、芯片、冲突)

语言:英文

金额:5积分

HSBC-中国房地产和物业管理行业2022年展望-2021.11.9-75页

3480

类型:行研

上传时间:2021-11

标签:投行报告、房地产、物业)

语言:英文

金额:5积分

汇丰-中国汽车芯片

3092

类型:行研

上传时间:2022-07

标签:汽车、芯片、投行报告)

语言:英文

金额:5积分

兰德公司3万字报告:美国与中国战争的军事胜利理论(中英对照)

2994

类型:国际关系

上传时间:2024-03

标签:台湾地区、中美战争、对华战略)

语言:中英

金额:10元

国际危机组织3万字报告:加强美中危机管理 (中英对照)

2864

类型:国际关系

上传时间:2022-06

标签:中美、危机管理、台湾地区)

语言:中英

金额:5元

疯狂!拜登扬言“武力护台”(中英对照全文)

2733

类型:国际关系

上传时间:2022-05

标签:美日、台湾地区)

语言:中英

金额:3元

HSBC-全球投资策略之未来城市:城市化形态的变化-2021.4-54页

2378

类型:策略

上传时间:2021-05

标签:投行报告、未来城市、城市化)

语言:英文

金额:5积分

瑞信-2021年全球财富报告(英)

2343

类型:专题

上传时间:2021-06

标签:全球财富、投行报告)

语言:英文

金额:5积分

积分充值

30积分

6.00元

90积分

18.00元

150+8积分

30.00元

340+20积分

68.00元

640+50积分

128.00元

990+70积分

198.00元

1640+140积分

328.00元

微信支付

余额支付

积分充值

应付金额:

0 元

请登录,再发表你的看法

登录/注册