微信扫一扫联系客服

微信扫描二维码

进入报告厅H5

关注报告厅公众号

At the end of my suffering there was a doo

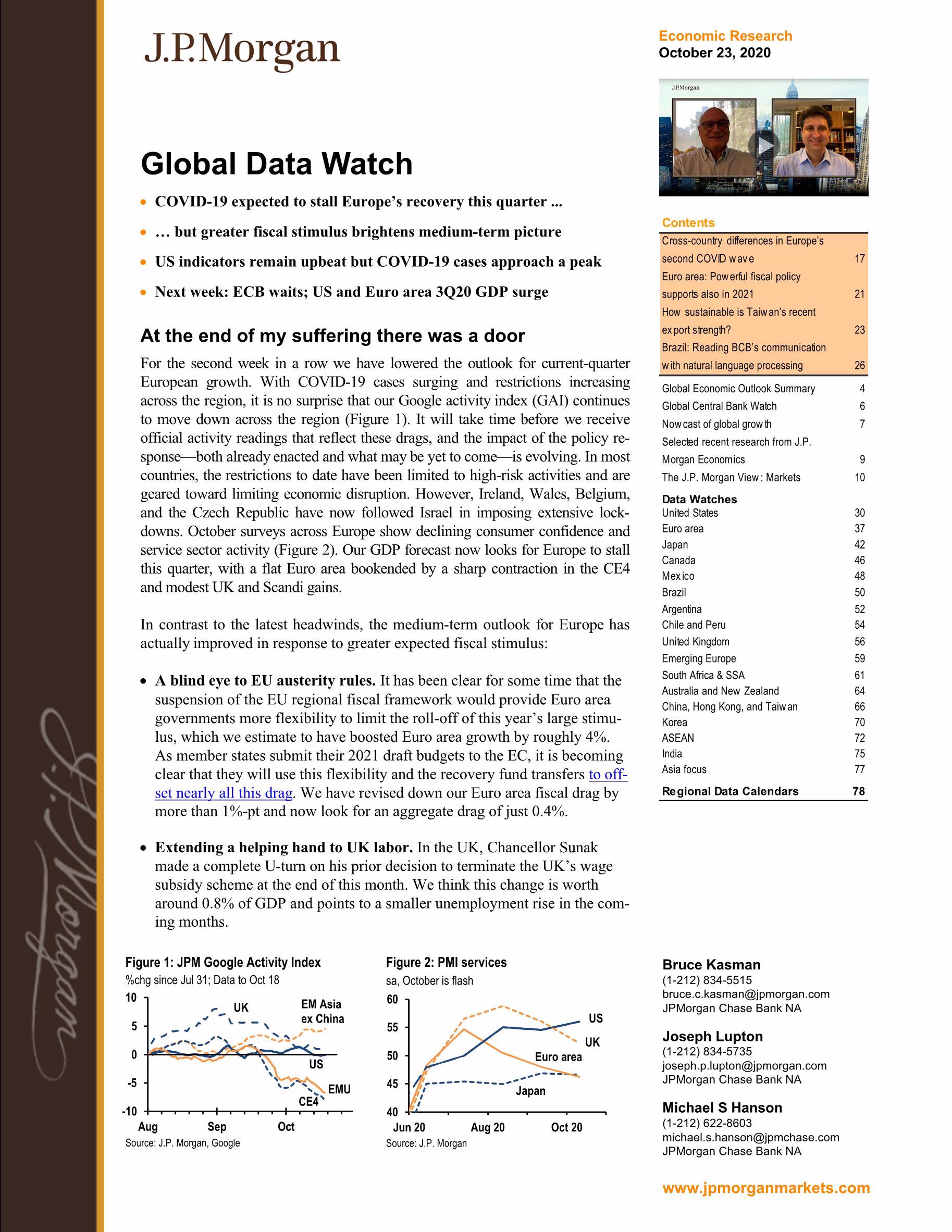

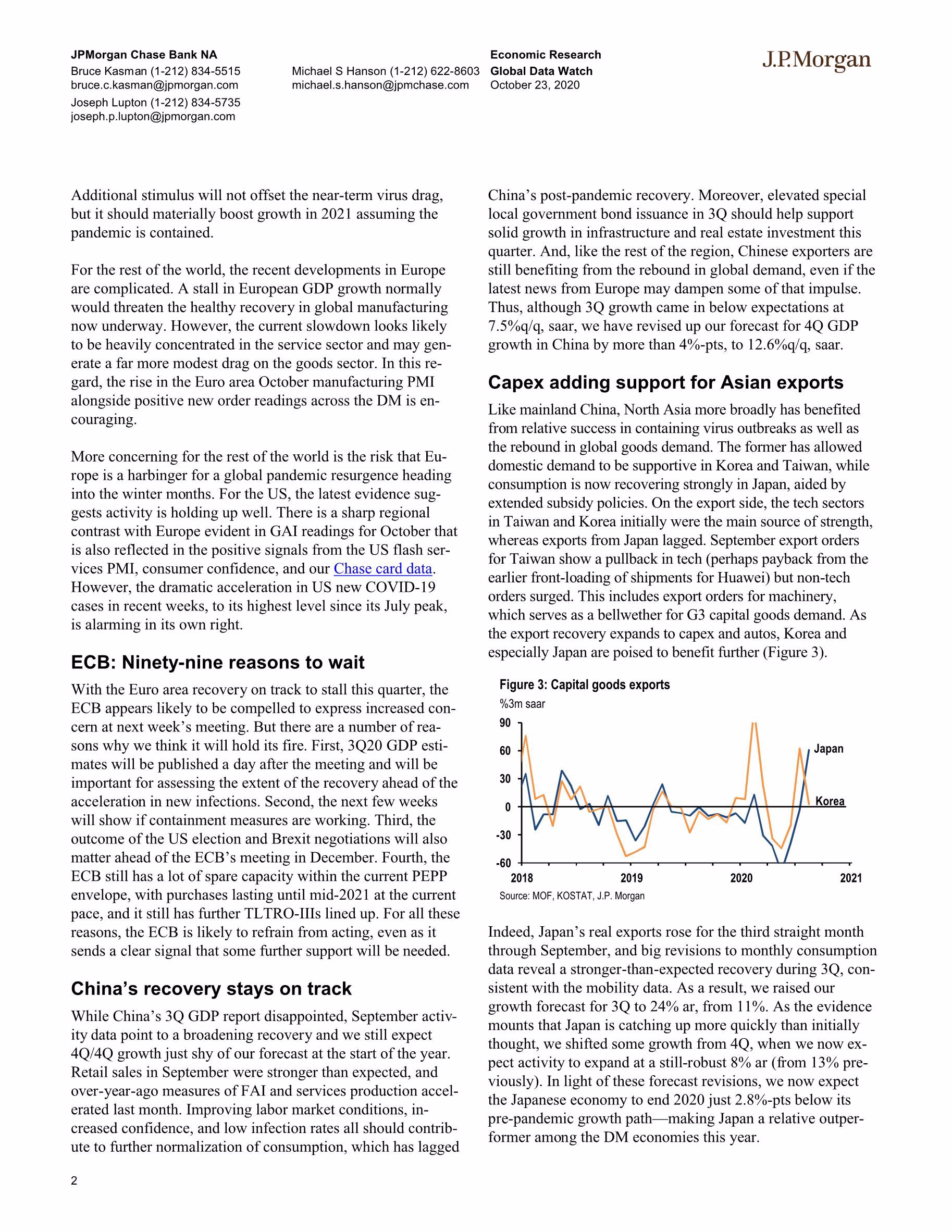

For the second week in a row we have lowered the outlook for current-quarter European growth. With COVID-19 cases surging and restrictions increasing across the region, it is no surprise that our Google activity index (GAI) continues to move down across the region (Figure 1). It will take time before we receive official activity readings that reflect these drags, and the impact of the policy response— both already enacted and what may be yet to come—is evolving. In most countries, the restrictions to date have been limited to high-risk activities and are geared toward limiting economic disruption. However, Ireland, Wales, Belgium, and the Czech Republic have now followed Israel in imposing extensive lockdowns. October surveys across Europe show declining consumer confidence and service sector activity (Figure 2). Our GDP forecast now looks for Europe to stall this quarter, with a flat Euro area bookended by a sharp contraction in the CE4 and modest UK and Scandi gains.

In contrast to the latest headwinds, the medium-term outlook for Europe has actually improved in response to greater expected fiscal stimulus:

A blind eye to EU austerity rules. It has been clear for some time that the suspension of the EU regional fiscal framework would provide Euro area governments more flexibility to limit the roll-off of this year’s large stimulus, which we estimate to have boosted Euro area growth by roughly 4%. As member states submit their 2021 draft budgets to the EC, it is becoming clear that they will use this flexibility and the recovery fund transfers to offset nearly all this drag. We have revised down our Euro area fiscal drag by more than 1%-pt and now look for an aggregate drag of just 0.4%.

Extending a helping hand to UK labor. In the UK, Chancellor Sunak made a complete U-turn on his prior decision to terminate the UK’s wage subsidy scheme at the end of this month. We think this change is worth around 0.8% of GDP and points to a smaller unemployment rise in the coming months.

相关报告

高盛中国市场策略-2022市场展望:“不适”的上行空间;离岸市场重回超配

5353

类型:策略

上传时间:2021-11

标签:投行报告、中国、市场展望)

语言:中文

金额:5积分

国际投行报告-全球芯片行业:芯片的冲突-台积电、三星和英特尔(英)

3974

类型:行研

上传时间:2022-06

标签:投行报告、芯片、冲突)

语言:英文

金额:5积分

HSBC-中国房地产和物业管理行业2022年展望-2021.11.9-75页

3501

类型:行研

上传时间:2021-11

标签:投行报告、房地产、物业)

语言:英文

金额:5积分

汇丰-中国汽车芯片

3117

类型:行研

上传时间:2022-07

标签:汽车、芯片、投行报告)

语言:英文

金额:5积分

HSBC-全球投资策略之未来城市:城市化形态的变化-2021.4-54页

2380

类型:策略

上传时间:2021-05

标签:投行报告、未来城市、城市化)

语言:英文

金额:5积分

瑞信-2021年全球财富报告(英)

2343

类型:专题

上传时间:2021-06

标签:全球财富、投行报告)

语言:英文

金额:5积分

瑞信-2022全球投资展望:股票、地区和宏观-2021.11.17-194页

1737

类型:宏观

上传时间:2021-11

标签:投行报告、2022投资展望、宏观经济)

语言:英文

金额:5积分

瑞信-全球财富报告2020-2020.10-56页

1549

类型:专题

上传时间:2020-10

标签:全球财富、投行报告)

语言:英文

金额:5积分

瑞信-全球半导体行业:中国集成电路产业的不均衡崛起-2021.1.20-184页

1511

类型:行研

上传时间:2021-01

标签:半导体、中国集成电路、投行报告)

语言:英文

金额:5积分

瑞信-中国能源行业-中国氢能源:如何更好地发挥中国氢主题-2021.3.15-118页

1298

类型:行研

上传时间:2021-03

标签:能源、氢能源、投行报告)

语言:英文

金额:5积分

积分充值

30积分

6.00元

90积分

18.00元

150+8积分

30.00元

340+20积分

68.00元

640+50积分

128.00元

990+70积分

198.00元

1640+140积分

328.00元

微信支付

余额支付

积分充值

应付金额:

0 元

请登录,再发表你的看法

登录/注册