微信扫一扫联系客服

微信扫描二维码

进入报告厅H5

关注报告厅公众号

Greater China ecosystem in-depth. In a follow-on to our China semiconductor reports, including China’s ascent and supply chain localisation, this report updates on the US-China policy implications, China’s manufacturing, design and tech supply chain, and the fabless industry map. Leveraging our full global semis team, we also take an in-depth look at equipment, materials, RF, Power, CPU, national IC fund investments, China fab projects, and profile 21 covered and Not Covered China IC companies’ business overview, drivers, near-term outlook, and valuation.

Semiconductors strategic importance rises. The semiconductor industry at US$450 bn and growing at a 6% CAGR since 2001 and rising as % of GDP is critical to the US$2 tn electronic market and strategic areas of cloud computing, 5G, network infrastructure, AI, and IoT. COVID-19 has only accelerated the digitisation trends and the importance of domestic self-sufficient supply chains, in contrast to the industry’s traditional global chain.

The US is looking to protect its leading 48% share consisting of its leading IDMs, fabless, equipment and EDA/IP, while China is looking to gain self-sufficiency and increase its 5% share, which lags its 20-25% share of tech demand and 30-40% hardware share.

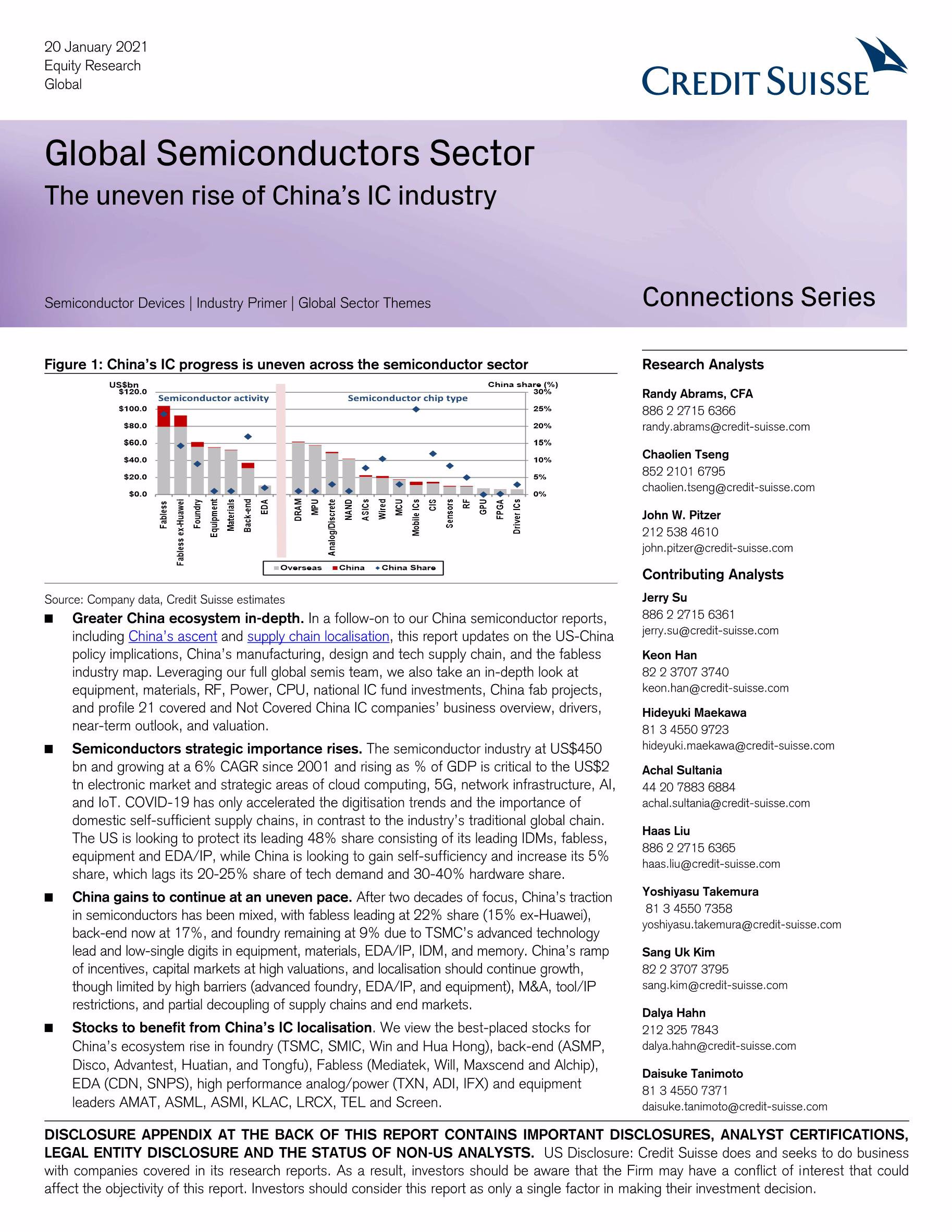

China gains to continue at an uneven pace. After two decades of focus, China’s traction in semiconductors has been mixed, with fabless leading at 22% share (15% ex-Huawei), back-end now at 17%, and foundry remaining at 9% due to TSMC’s advanced technology lead and low-single digits in equipment, materials, EDA/IP, IDM, and memory. China’s ramp of incentives, capital markets at high valuations, and localisation should continue growth, though limited by high barriers (advanced foundry, EDA/IP, and equipment), M&A, tool/IP restrictions, and partial decoupling of supply chains and end markets.

Stocks to benefit from China’s IC localisation. We view the best-placed stocks for China’s ecosystem rise in foundry (TSMC, SMIC, Win and Hua Hong), back-end (ASMP, Disco, Advantest, Huatian, and Tongfu), Fabless (Mediatek, Will, Maxscend and Alchip), EDA (CDN, SNPS), high performance analog/power (TXN, ADI, IFX) and equipment leaders AMAT, ASML, ASMI, KLAC, LRCX, TEL and Screen.

相关报告

173页中国半导体深度报告:牛角峥嵘-20210406-国盛证券-173页

7405

类型:行研

上传时间:2021-04

标签:半导体)

语言:中文

金额:5积分

美国智库万字报告:限制中国对人工智能未来的准入 (中英对照)

7364

类型:国际关系

上传时间:2022-10

标签:AI、半导体、芯片技术)

语言:中英

金额:3元

最新翻译1.9万字!《欧洲芯片法案》-中英对照

6953

类型:法律合同

上传时间:2022-02

标签:芯片法案、数字化、半导体)

语言:中英

金额:7元

汽车半导体研究框架-2020.12-方正证券-123页

6587

类型:行研

上传时间:2021-02

标签:汽车、半导体)

语言:中文

金额:5积分

美国智库3文字报告:半导体与为地缘政治服务的供应链监管(中英文版)

6328

类型:行研

上传时间:2021-09

标签:半导体、供应链监管)

语言:中英

金额:7元

半导体行业:半导体产业链全景梳理-20211213-长城证券-34页

6228

类型:行研

上传时间:2021-12

标签:半导体、产业链)

语言:中文

金额:免费

美国智库1.2万字报告:2021美国国家半导体行业报告(中英文版)

5768

类型:行研

上传时间:2021-10

标签:半导体、芯片短缺)

语言:中英

金额:5元

欧洲智库4万字报告:大国竞争时期的半导体和关键原材料生态系统 (中英对照)

5605

类型:国际关系

上传时间:2022-10

标签:半导体、原材料、大国竞争)

语言:中英

金额:7元

ChatGPT对GPU算力的需求测算与相关分析

5454

类型:专题

上传时间:2023-02

标签:ChatGPT、GPU、半导体)

语言:中文

金额:5积分

高盛中国市场策略-2022市场展望:“不适”的上行空间;离岸市场重回超配

5353

类型:策略

上传时间:2021-11

标签:投行报告、中国、市场展望)

语言:中文

金额:5积分

积分充值

30积分

6.00元

90积分

18.00元

150+8积分

30.00元

340+20积分

68.00元

640+50积分

128.00元

990+70积分

198.00元

1640+140积分

328.00元

微信支付

余额支付

积分充值

应付金额:

0 元

请登录,再发表你的看法

登录/注册