微信扫一扫联系客服

微信扫描二维码

进入报告厅H5

关注报告厅公众号

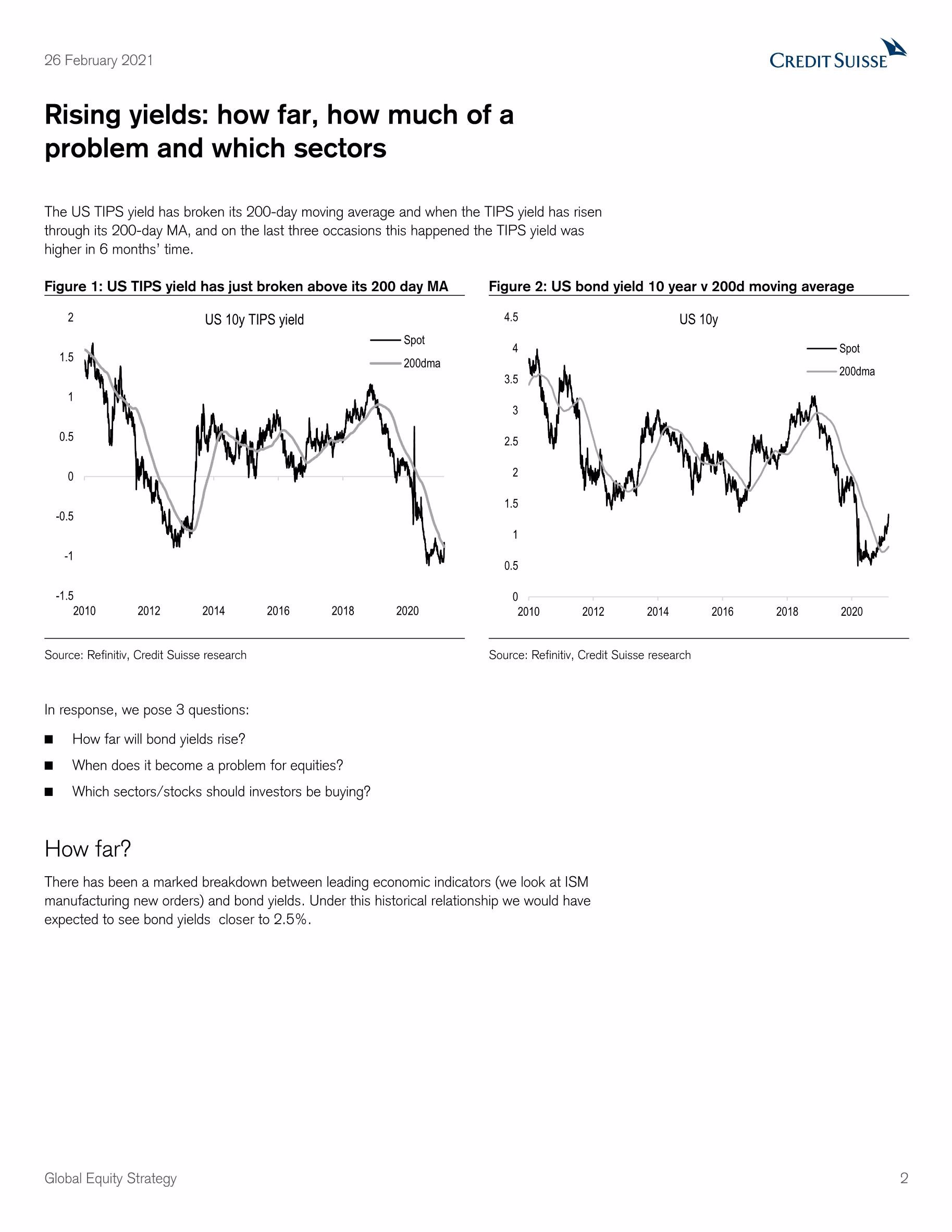

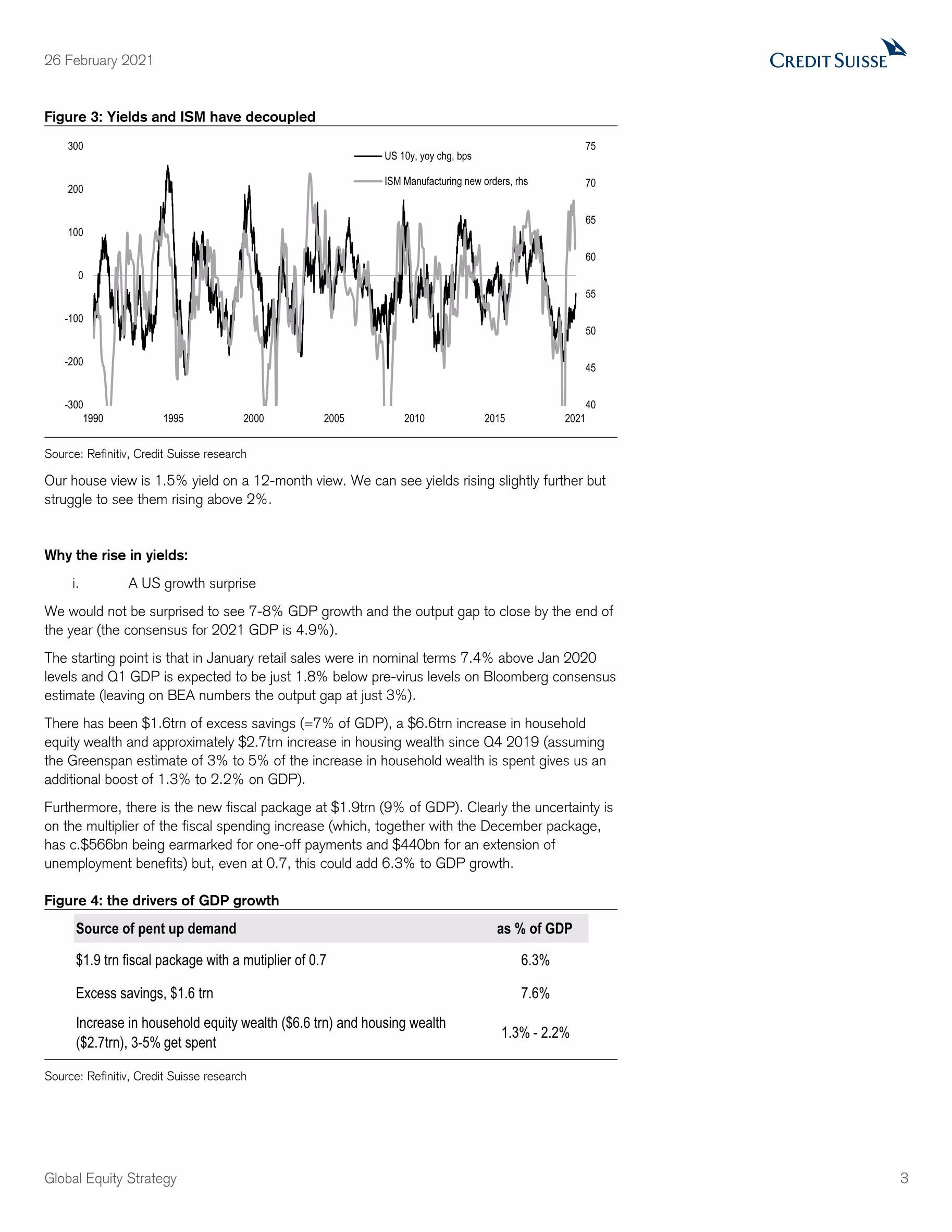

On the global strategy team we can see the 10 year potentially rising to 1.8-2% based on: an extreme gap between ISM and bond yields, the risk that US GDP is c7-8% rather than consensus of c5% on the back of fiscal packages, c$9.3trn in real wealth generated since Jan 20 and $1.5trn of excess savings - thus we could see the output gap closing in Q4. We see inflation expectations rising to 2.5%-3% eventually (from c.2.15% currently), see Inflation – the big issue, Jan 29, with prices paid suggesting a sharp rise in core PCE and wage growth starting to rise; and the Fed only buying a third of net issuance.

What caps the rise in yields: i) a limited rise in European or JGB yields and an increasingly attractive (currency hedged) yield pick-up in US yields; ii) the Fed may use forward guidance to cap rates (we think it will not want to see that much of a rise with the average maturity of mortgage debt more than 10 years and IG debt c9 years, thus 1% on yield could take 1.5% to 2% off GDP growth). Critically, we see most of the move higher being driven by inflation expectations.

What is problem level for equities? Around 2% for the 10y UST, in our view. Historically, equities have been able to accommodate an average 130bp rise in rates with 170bps seen in 08/09. Higher rates hurt equities via valuation, interest charge, growth and funds flow. We don’t see rising inflation expectations as a problem until the Fed meets its target (probably around core CPI of c2.8%) and historically equities have not de-rated until inflation is above 3%. The key driver of multiples in the past 5 years has been the TIPS yield (prior to that it was not).

Regions: Japan is the biggest winner from the rise in nominal yields or TIPs. GEM is most vulnerable though with their basic balance of payments at a 15 year high they are much less vulnerable than during the taper tantrum. The US is now more vulnerable to a rise in TIPS given its high exposure to long duration assets. Italy & Spain have been the best-performing countries when yields rise, Switzerland and the US the worst.

Sectors: Unsurprisingly, real estate, utilities, and beverages have the most negative correlation to rising bond yields. Banks, diversified financials, and autos the most positive. Higher yields are pro-cyclical, but we keep to our benchmark of non-financials because they are pricing in a PMI in the low 70s (5.5% European GDP) and we have had the equal-largest cyclical rally on record. In the past 2 years US tech has been very driven by the TIPS yield (a rise leads to long duration assets underperforming). We add to our overweight of banks (we have 22% upside on our model, more so on our year-end forecasts), add to life companies and further reduce the sizes of our tech (ex-semis) and utilities overweights.

Stocks: We look at the stocks most positively correlated to rising bond yields and Outperform rated by our analysts, including ING, Lloyds, AXA, BASF and Randstad. Stocks with high debt to market cap (with poor FCF) and are negatively correlated to bond yields include UU, ABI and Italgas.

相关报告

高盛中国市场策略-2022市场展望:“不适”的上行空间;离岸市场重回超配

5353

类型:策略

上传时间:2021-11

标签:投行报告、中国、市场展望)

语言:中文

金额:5积分

国际投行报告-全球芯片行业:芯片的冲突-台积电、三星和英特尔(英)

3974

类型:行研

上传时间:2022-06

标签:投行报告、芯片、冲突)

语言:英文

金额:5积分

HSBC-中国房地产和物业管理行业2022年展望-2021.11.9-75页

3502

类型:行研

上传时间:2021-11

标签:投行报告、房地产、物业)

语言:英文

金额:5积分

汇丰-中国汽车芯片

3117

类型:行研

上传时间:2022-07

标签:汽车、芯片、投行报告)

语言:英文

金额:5积分

HSBC-全球投资策略之未来城市:城市化形态的变化-2021.4-54页

2380

类型:策略

上传时间:2021-05

标签:投行报告、未来城市、城市化)

语言:英文

金额:5积分

瑞信-2021年全球财富报告(英)

2343

类型:专题

上传时间:2021-06

标签:全球财富、投行报告)

语言:英文

金额:5积分

瑞信-2022全球投资展望:股票、地区和宏观-2021.11.17-194页

1737

类型:宏观

上传时间:2021-11

标签:投行报告、2022投资展望、宏观经济)

语言:英文

金额:5积分

瑞信-全球财富报告2020-2020.10-56页

1549

类型:专题

上传时间:2020-10

标签:全球财富、投行报告)

语言:英文

金额:5积分

瑞信-全球半导体行业:中国集成电路产业的不均衡崛起-2021.1.20-184页

1511

类型:行研

上传时间:2021-01

标签:半导体、中国集成电路、投行报告)

语言:英文

金额:5积分

瑞信-中国能源行业-中国氢能源:如何更好地发挥中国氢主题-2021.3.15-118页

1298

类型:行研

上传时间:2021-03

标签:能源、氢能源、投行报告)

语言:英文

金额:5积分

积分充值

30积分

6.00元

90积分

18.00元

150+8积分

30.00元

340+20积分

68.00元

640+50积分

128.00元

990+70积分

198.00元

1640+140积分

328.00元

微信支付

余额支付

积分充值

应付金额:

0 元

请登录,再发表你的看法

登录/注册