微信扫一扫联系客服

微信扫描二维码

进入报告厅H5

关注报告厅公众号

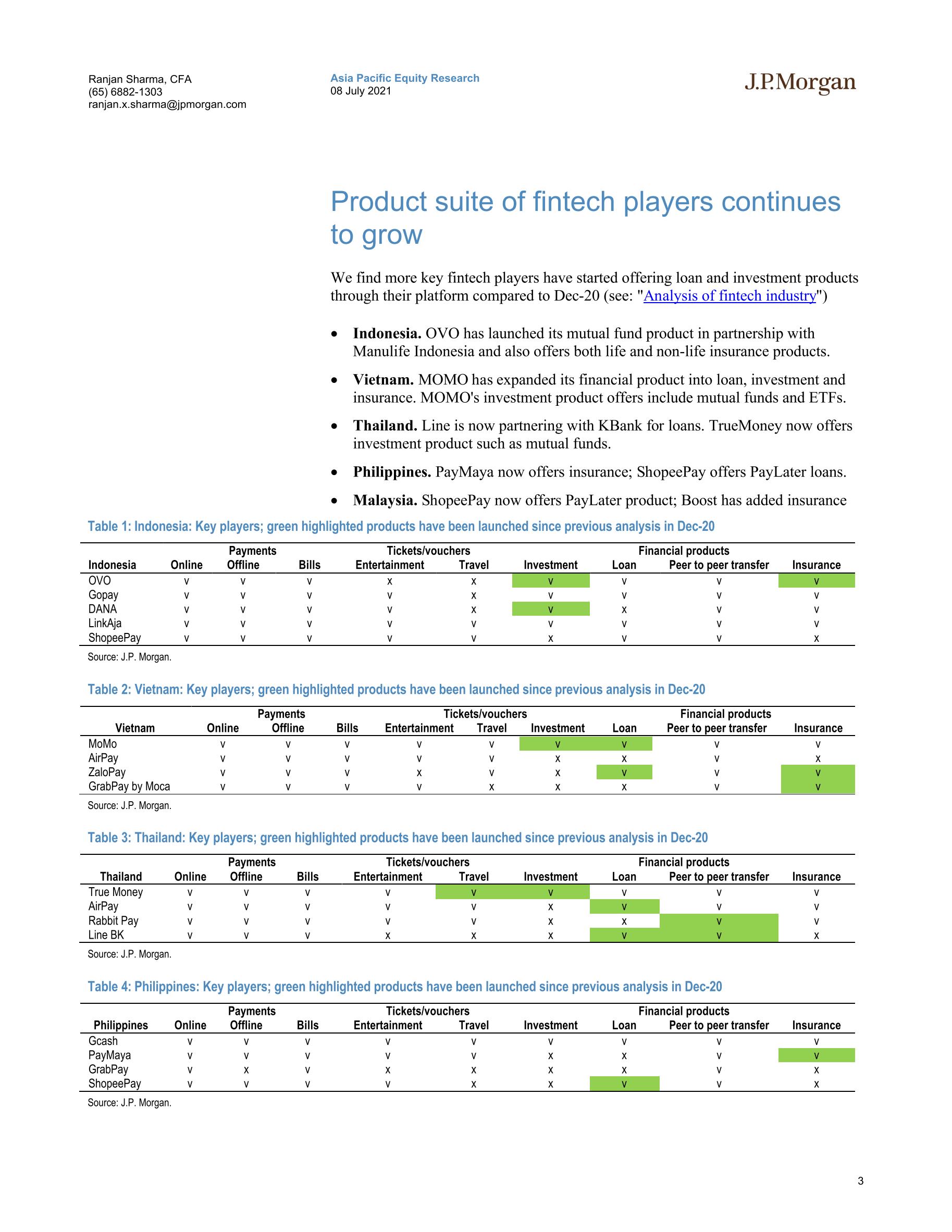

We analyze the economics of the fintech industry pursuant to strong investor interest. With rich merchant discount rates (MDRs) and low cost of funds, online payments are currently lucrative for e-wallets at gross profit level.

Online lending continues to proliferate with conventional loan products carrying annualized interest rates of 12%-60%. Introduction of Afterpaystyled interest-free customer loans can drive rapid loan growth while being high profitable and containing risks for everyday platforms like SE/Shopee.

Licensed digital banks are offering up to 4pp higher deposit rates vs.

traditional banks and it is to be seen whether this can overcome the trust differential vs. established banks.

Online payments lucrative for issuers at gross profit level. Our analysis shows MDRs for online payments using e-wallets are between 1.5% and 3.3% – at a premium to offline MDRs, bank transfers, and even debit cards in some cases. Our discussions with regional acquirers indicate issuers like e-wallets typically keep at least 50% of the MDRs. The rich MDRs compare to cost of funds as low as $0.10/transaction – implying online payments are lucrative at gross profit level. However, elevated S&M expense weighs on industry profitability. Regulation presents downside risks to online MDRs though regulators have so far focused mainly on offline MDRs.

Online lending continues to proliferate. ASEAN has seen more fintech companies add online lending products. Interest rates on loans remain relatively high at annualized rates of 12%-60% (Tables 7-10). Digital banks have been licensed in Indonesia, the Philippines and Singapore and we find deposit rate differential of up to 4pp. The attractiveness of online lending will eventually depend on the effectiveness of the risk management systems.

Afterpay-style loans present material revenue opportunity while containing risks for platforms. Platforms have introduced Afterpay style products: 1) activated through the app, 2) interest-free loans to eligible customers which can pay bills in 4 monthly installments, 3) interest is charged in the form of MDRs to merchants, and 4) consumer pays an admin fees on missed payments. Our Python-driven scenario analysis indicates these products present material opportunity for platforms. For example, with $1bn capital, average order value of $50, loan duration of 4 months, and 5% interest rate, a fintech can theoretically extend loans worth $5bn and generate returns of 27% in 12 months. A low default rate can increase the effective returns (vs. no defaults) due to the relatively high admin fees. At 5% default rate with $10 admin fees, the effective earnings increase to 28%.

The long tail of the micro-loans extended over apps that customers rely on every day can limit default rate and increase recovery rates, in our view.

Implications for SE and Indonesian banks: The material revenue opportunity of payments will likely be visible as off-platform use of ShopeePay grows. We anticipate financial services revenues to grow rapidly over the next five years driven by payments (TAM: >$1.5tn by TPV), online lending and distribution of financial products. The profitability of the Indonesian Big4 banks is set to be structurally eroded in the next 3-5 years.

相关报告

蚂蚁集团:2021全球10大金融科技趋势

7088

类型:行研

上传时间:2020-10

标签:金融科技、蚂蚁集团)

语言:中文

金额:5积分

高盛中国市场策略-2022市场展望:“不适”的上行空间;离岸市场重回超配

5357

类型:策略

上传时间:2021-11

标签:投行报告、中国、市场展望)

语言:中文

金额:5积分

中国领先金融科技TOP50

5305

类型:数据榜单

上传时间:2021-01

标签:金融科技、TOP0)

语言:中文

金额:5积分

Fintech2030:全球金融科技生态扫描

5122

类型:专题

上传时间:2021-06

标签:金融科技、生态扫描)

语言:中文

金额:5积分

金融科技创新发展研究报告

4774

类型:专题

上传时间:2020-11

标签:金融科技、创新)

语言:中文

金额:5积分

J.P. 摩根-2021全球金融科技行业报告:区块链、比特币和数字金融-2021.2.18-86页

4190

类型:行研

上传时间:2021-02

标签:金融科技、区块链、比特币)

语言:英文

金额:5积分

《金融科技推动中国绿色金融发展:案例与展望(2021)》

4135

类型:专题

上传时间:2021-06

标签:金融科技、绿色金融、展望)

语言:中文

金额:5积分

中关村互联网金融研究院-中国金融科技和数字普惠金融发展报告(2022)

4123

类型:行研

上传时间:2022-03

标签:金融科技、数字普惠、发展)

语言:中文

金额:5积分

中国金融科技年度报告2020

4089

类型:行研

上传时间:2021-01

标签:金融科技、年度报告)

语言:中文

金额:5积分

国际投行报告-全球芯片行业:芯片的冲突-台积电、三星和英特尔(英)

3975

类型:行研

上传时间:2022-06

标签:投行报告、芯片、冲突)

语言:英文

金额:5积分

积分充值

30积分

6.00元

90积分

18.00元

150+8积分

30.00元

340+20积分

68.00元

640+50积分

128.00元

990+70积分

198.00元

1640+140积分

328.00元

微信支付

余额支付

积分充值

应付金额:

0 元

请登录,再发表你的看法

登录/注册