微信扫一扫联系客服

微信扫描二维码

进入报告厅H5

关注报告厅公众号

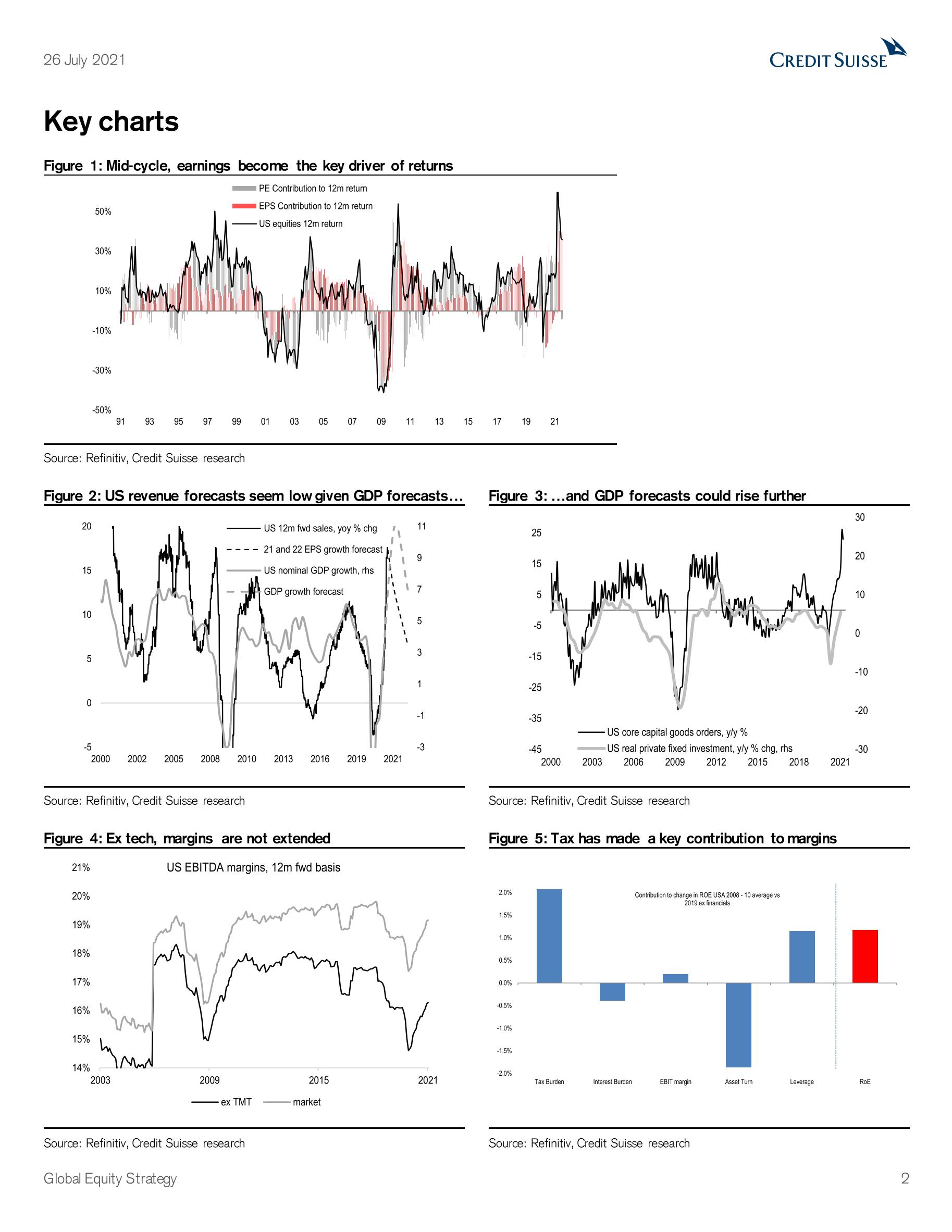

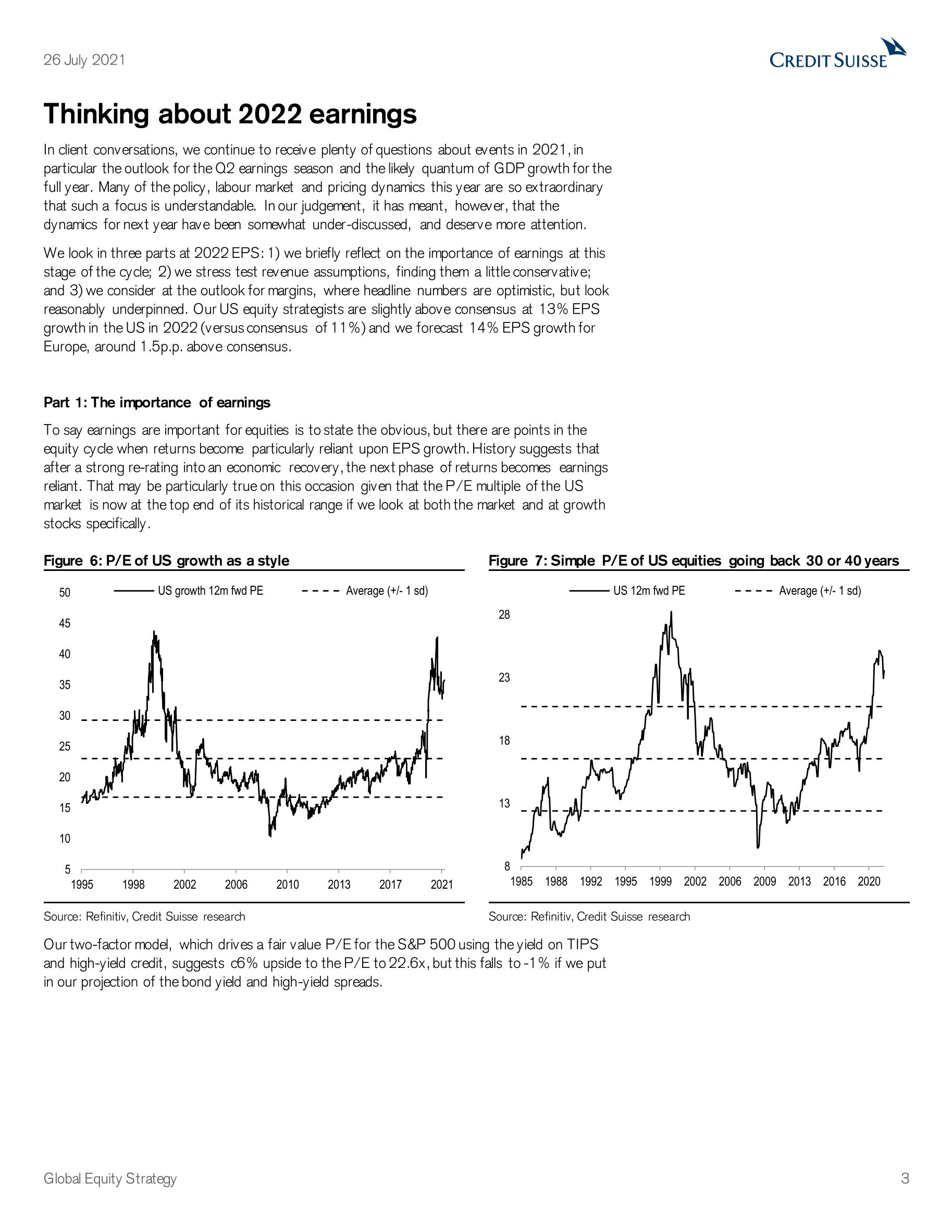

Entering the stage of the cycle at which earnings are key: Progression into a mid-cycle stage tends to see markets become more earnings-driven, with the case for further valuation upside for equities now limited. Our two-factor US P/E model, driven by TIPS and credit spreads, points to c.6% upside, falling to -1% once we adjust for our yield forecasts. While that may mean more muted returns than seen ov er the past 12 months, it is not a cause for pessimism: we agree with our US team and see consensus EPS estimates as being too low for next year. Our US team forecasts 13% EPS growth at US$225 for 2022, versus consensus of 11.5% at US$210). The following factors support this: Scope for revenue growth estimates to move higher, if anything S&P revenue growth tends to move with a beta of roughly 2 to GDP growth, and we think consensus revenue growth should be closer to 9% than the current 6%. There is a surprisingly large dispersion of forecasts for US GDP growth next year; we expect GDP to come in ahead of a median consensus expectation of 4.1%. Private sector dissaving should ultimately offset public-sector tightening. Excess household sav ings account for 12% of GDP, and there has been a $14trn positive wealth effect , which should more than offset fiscal tightening of c4% of GDP. We think supply-side constraints are temporary (with a true unemployment rate of c8% according to Fed Chair Jerome Powell). Falling bonds yields help housing, corporates’ investment should ramp up and the bulk of tightening in China should be behind us.

Margin estimates are less aggressive than they appear under the surface Consensus forecasts margins to rise to an all-time high of 13.5%, while the profit share of GDP is at only normal levels, which is an unusual decoupling. However, on an EBITDA margin basis and excluding tech, margins are only in the middle of their 10-year range. Tax and interest have been the two key drivers of net margins (with tax and leverage being the main drivers of RoE): the interest charge should fall (reflecting the fall in corporate debt) , and as we discuss below, tax rises look limited. Tech margins appear underpinned owing to scale, rising capital intensity and the network effect.

We think margins can remain resilient as: i) there is no obvious overinvestment in either tech or the broader economy; ii) labour’s pricing power should be temporary. The profit share of GDP falls if the labour share of GDP rises, but with a likely true unemployment rate of c8%, wage growth pressure should dissipate once additional unemployment benefits end in September. iii) When PPI inflation is above CPI, 70% of the time margins have risen.

Tax increases may be less of an issue than expected Under a worst-case scenario for earnings, a rise in the statutory tax rate from 21% to 28% would take around 6-7pp off EPS growth, according to our US strategy colleagues (taking their estimate down to 8% for 2022). However, moderate Democrats have come out in favour of a rise to 25%, and firms have a number of mitigation measures they can take. The Global Minimum Corporate tax rate is expected to raise about $150bn, or about 3% of global profits. In our experience, the impact of higher taxation on earnings tends to be overestimated by the market.

Thus, for 2022 we assume EPS growth of 13% in the US and 14% in Europe – around 1.5% above consensus in both cases – therefore we remain structurally positive on equities, though we see near-term reasons for consolidation (see Equities: a consolidation phase but we remain strategically positive, 28 May 2021).

相关报告

高盛中国市场策略-2022市场展望:“不适”的上行空间;离岸市场重回超配

5354

类型:策略

上传时间:2021-11

标签:投行报告、中国、市场展望)

语言:中文

金额:5积分

国际投行报告-全球芯片行业:芯片的冲突-台积电、三星和英特尔(英)

3974

类型:行研

上传时间:2022-06

标签:投行报告、芯片、冲突)

语言:英文

金额:5积分

HSBC-中国房地产和物业管理行业2022年展望-2021.11.9-75页

3504

类型:行研

上传时间:2021-11

标签:投行报告、房地产、物业)

语言:英文

金额:5积分

汇丰-中国汽车芯片

3122

类型:行研

上传时间:2022-07

标签:汽车、芯片、投行报告)

语言:英文

金额:5积分

HSBC-全球投资策略之未来城市:城市化形态的变化-2021.4-54页

2382

类型:策略

上传时间:2021-05

标签:投行报告、未来城市、城市化)

语言:英文

金额:5积分

瑞信-2021年全球财富报告(英)

2345

类型:专题

上传时间:2021-06

标签:全球财富、投行报告)

语言:英文

金额:5积分

瑞信-2022全球投资展望:股票、地区和宏观-2021.11.17-194页

1738

类型:宏观

上传时间:2021-11

标签:投行报告、2022投资展望、宏观经济)

语言:英文

金额:5积分

瑞信-全球财富报告2020-2020.10-56页

1549

类型:专题

上传时间:2020-10

标签:全球财富、投行报告)

语言:英文

金额:5积分

瑞信-全球半导体行业:中国集成电路产业的不均衡崛起-2021.1.20-184页

1512

类型:行研

上传时间:2021-01

标签:半导体、中国集成电路、投行报告)

语言:英文

金额:5积分

瑞信-中国能源行业-中国氢能源:如何更好地发挥中国氢主题-2021.3.15-118页

1298

类型:行研

上传时间:2021-03

标签:能源、氢能源、投行报告)

语言:英文

金额:5积分

积分充值

30积分

6.00元

90积分

18.00元

150+8积分

30.00元

340+20积分

68.00元

640+50积分

128.00元

990+70积分

198.00元

1640+140积分

328.00元

微信支付

余额支付

积分充值

应付金额:

0 元

请登录,再发表你的看法

登录/注册