微信扫一扫联系客服

微信扫描二维码

进入报告厅H5

关注报告厅公众号

We see regional strategy becoming more relevant, with regional dispersion in its 96th percentile.

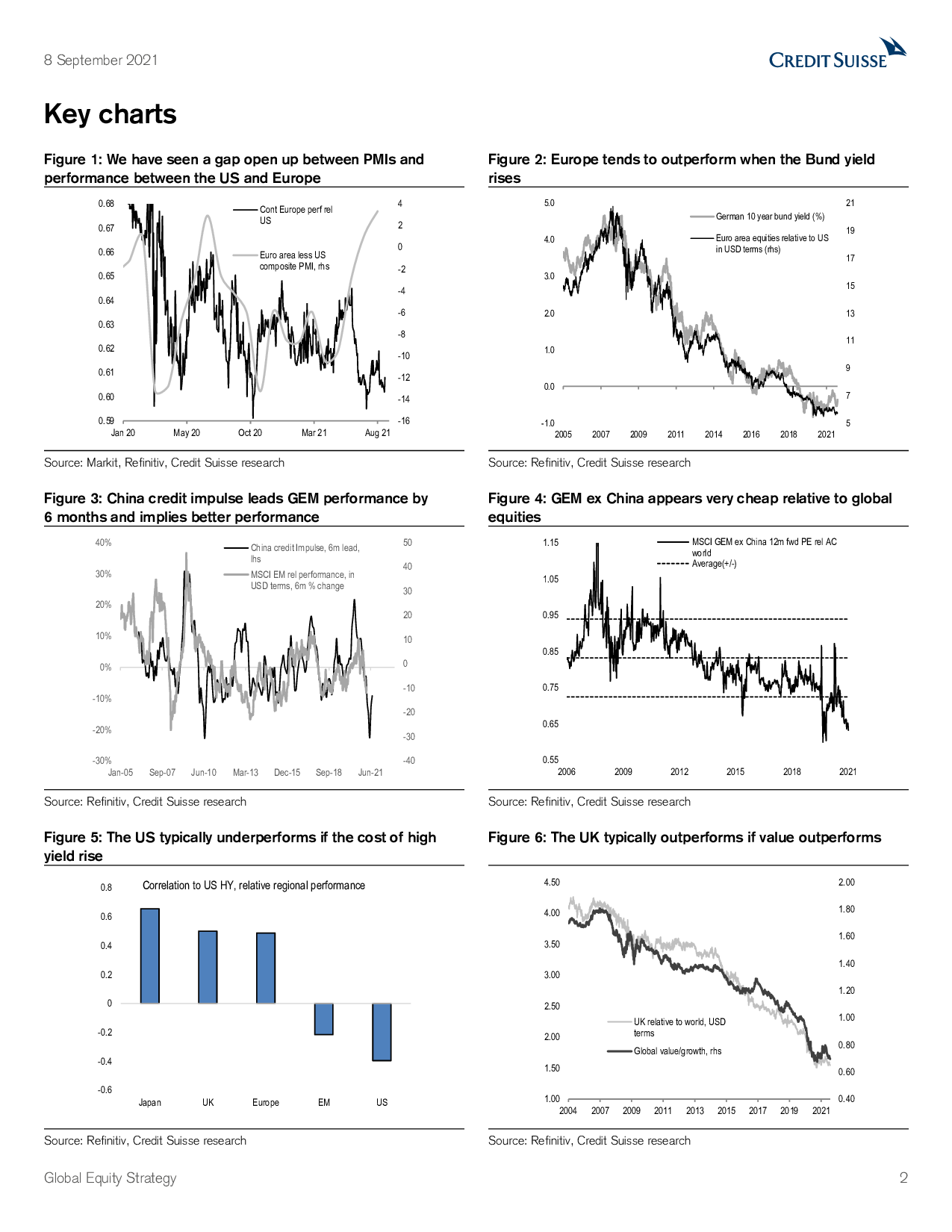

Macroeconomic backdrop/scorecard: Higher bond yields driven by higher US inflation expectations, IP accelerates despite PMIs falling with well above-trend growth in 2022, value outperforms in Europe and the US dollar looks close to the end of a bear-market rally. With these factors combined, our composite scorecard most favours Continental Europe and GEM.

Continental Europe remains our key overweight: 1) Macro: It is the only region where CS is above consensus for GDP in 2021 and 2022 – PMI momentum is much better than in the US, and markets have unusually decoupled from this. Rising inflation expectations/bond yields usually lead Europe to outperform. Europe has less labour backlog (or wage problems) than other regions. 2) Excess liquidity is the highest of any region as the ECB continues to expand its balance sheet more than anywhere else. 3) Valuation attractive (P/E 18% discount to US; actual ERP is 8.1% cf 6.5% warranted). 4) Positioning remains cautious. Strategically, Europe is well positioned because: it has structurally easier fiscal and monetary policy; the Eurosceptic parties’ popularity has fallen sharply; and Europe is dominant in green/sustainable companies (8% of market cap). We prefer Spain and Italy over Germany. Our ‘Top of the Crop’ ideas include BASF, Brenntag, Logitech, Schneider, SocGen and Smurfit Kappa.

GEM (ex-China)—raise to small overweight: GEM benefit from a weaker US dollar, rising inflation expectations and China PMIs now being close to lows (and China close to an easing cycle). China credit impulse leads GEM performance by six months. Equity and currency valuations (ex-China) are both close to 15-year lows. GEM equities have abnormally lagged behind GEM bonds (market-cap weighted). GEM risk appetite is 2std below its norm. We are benchmark China, but see much of the negative news priced in (P/E 27% discount to global markets). We particularly like India (our long-standing structural overweight), Mexico and South Korea and upgrade Taiwan to overweight.

UK—remain overweight: UK performance is more closely tied to value outperforming than any other region, and we think value outperforms in Europe. Valuations are extreme. Fiscal fundamentals are the best outside of Germany in the G7. The UK (along with Spain) has the highest catch-up potential in terms of GDP. The issue is likely sterling strength; therefore, we would be more overweight unhedged. We like domestic UK (M&S, Bellway). We see Unilever, Asos and Elementis also looking abnormally cheap versus their international peers.

Japan down to benchmark: Although most of this year’s headwinds are behind us (slowing China, falling TIPS, sharply rising oil, delayed vaccinations), we see nothing further compelling in Japan (valuation, corporate change, funds flow) at a time when the macro backdrop is not clearly supportive (Japan has the highest operational leverage to rising IP momentum, but we think global PMIs are likely to fall and the dollar weaken).

US—small underweight: The US tends to be the worst-performing region when the cost of high-yield debt rises (having relied on leverage more than any other region). It has the lowest operational leverage and therefore underperforms when non-US IP accelerates to be less above 3%. We are only a small overweight of tech (the US outperforms 70% of the time tech outperforms). Tax and regulation risk seem higher than in Europe or Japan. Valuations are extreme (ex TMT). The US comes bottom on our composite and our macro factor scorecards.

相关报告

高盛中国市场策略-2022市场展望:“不适”的上行空间;离岸市场重回超配

5353

类型:策略

上传时间:2021-11

标签:投行报告、中国、市场展望)

语言:中文

金额:5积分

国际投行报告-全球芯片行业:芯片的冲突-台积电、三星和英特尔(英)

3974

类型:行研

上传时间:2022-06

标签:投行报告、芯片、冲突)

语言:英文

金额:5积分

HSBC-中国房地产和物业管理行业2022年展望-2021.11.9-75页

3501

类型:行研

上传时间:2021-11

标签:投行报告、房地产、物业)

语言:英文

金额:5积分

汇丰-中国汽车芯片

3116

类型:行研

上传时间:2022-07

标签:汽车、芯片、投行报告)

语言:英文

金额:5积分

HSBC-全球投资策略之未来城市:城市化形态的变化-2021.4-54页

2380

类型:策略

上传时间:2021-05

标签:投行报告、未来城市、城市化)

语言:英文

金额:5积分

瑞信-2021年全球财富报告(英)

2343

类型:专题

上传时间:2021-06

标签:全球财富、投行报告)

语言:英文

金额:5积分

瑞信-2022全球投资展望:股票、地区和宏观-2021.11.17-194页

1737

类型:宏观

上传时间:2021-11

标签:投行报告、2022投资展望、宏观经济)

语言:英文

金额:5积分

瑞信-全球财富报告2020-2020.10-56页

1549

类型:专题

上传时间:2020-10

标签:全球财富、投行报告)

语言:英文

金额:5积分

瑞信-全球半导体行业:中国集成电路产业的不均衡崛起-2021.1.20-184页

1511

类型:行研

上传时间:2021-01

标签:半导体、中国集成电路、投行报告)

语言:英文

金额:5积分

瑞信-中国能源行业-中国氢能源:如何更好地发挥中国氢主题-2021.3.15-118页

1298

类型:行研

上传时间:2021-03

标签:能源、氢能源、投行报告)

语言:英文

金额:5积分

积分充值

30积分

6.00元

90积分

18.00元

150+8积分

30.00元

340+20积分

68.00元

640+50积分

128.00元

990+70积分

198.00元

1640+140积分

328.00元

微信支付

余额支付

积分充值

应付金额:

0 元

请登录,再发表你的看法

登录/注册