微信扫一扫联系客服

微信扫描二维码

进入报告厅H5

关注报告厅公众号

We go from Goldilocks to steady-state expansion. Growth broadens out. Inflation rises but does not get out of hand.

Policy normalises but does not get disruptive.

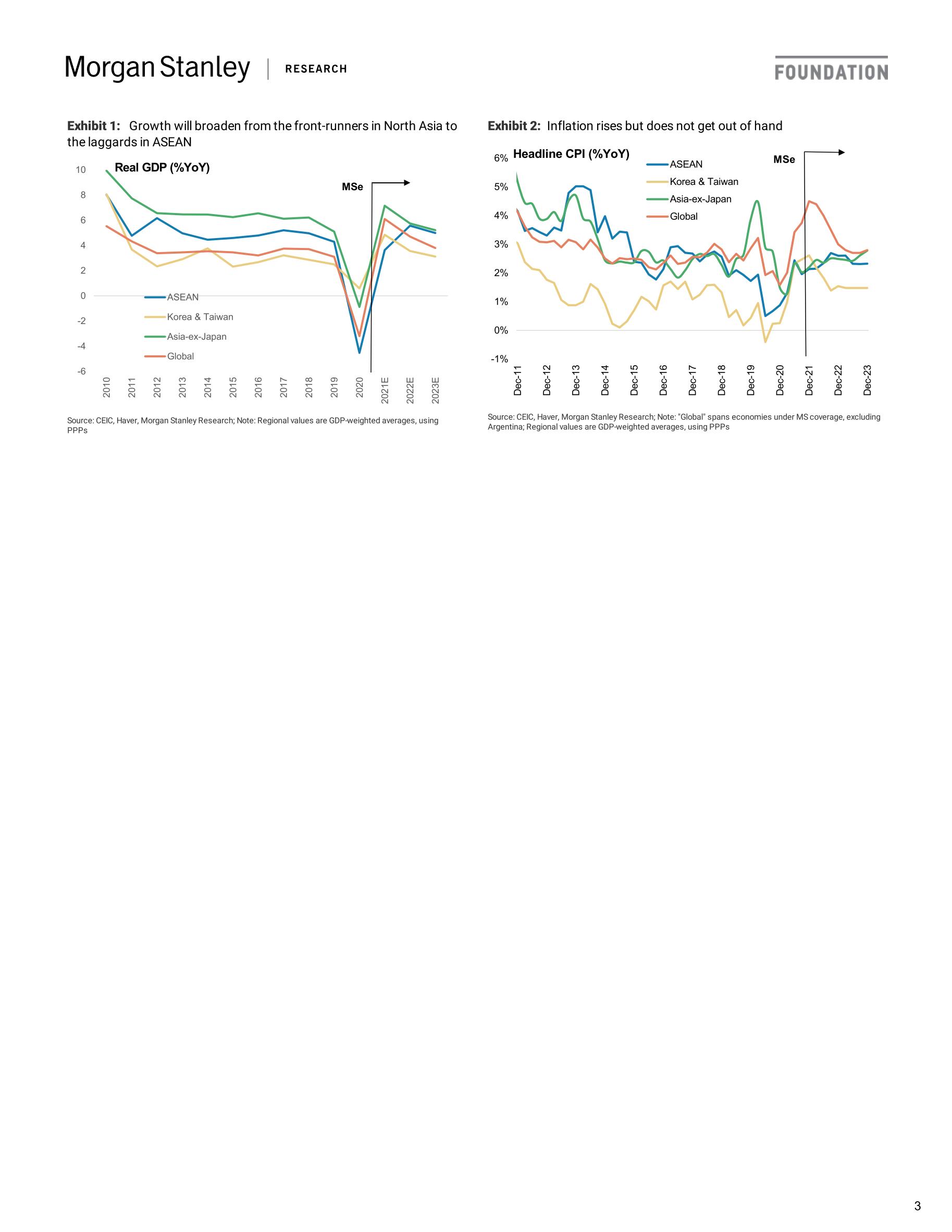

Fret not, we are going from Goldilocks to steady-state expansion Stagflation concerns have emerged given China's deleveraging and global supplyside constraints. We are not in the stagflation camp and believe our coverage region is advancing from a Goldilocks scenario to steady-state expansion. In the latter, growth broadens out from the front-runners to the laggards and from exports to domestic demand. Inflation rises but does not get out of hand. Policy normalises but does not get disruptive. ASEAN is better placed than North Asia as growth accelerates and growth differentials get more favourable.

The "stag" part of stagflation holds no water; Firmly in an expansionary phase Normalisation in one-off tech demand and China's deleveraging do not portend a cliff-drop in exports. Secular tech demand remains given digitalisation/automation. China's countercyclical easing and the US' procyclical stimulus mean that even as export growth moderates, it will remain at abovetrend levels. Rising vaccination rates enable growth to broaden from exports to domestic demand. We see policymakers implementing enough doses to fully vaccinate ~90% and more of the total population in our coverage region by Mar22. The need to alleviate supply constraints is also leading to capex expansion in Korea and Taiwan.

Inflation rises but does not get out of hand Supply constraints have led to higher input costs and are driven by structural (decarbonisation, truck driver shortages), cyclical (strong recovery) and temporary factors (weather, Covid production disruptions and capex delays).

Structural factors are unlikely to go away but temporary factors should fade and alleviate constraints. MS price forecasts for commodities/semis show peak inflation is mostly behind us. Labour constraints in our region are not as stark as in the US. Besides, most economies are still closing a negative output gap. The spillover of higher input costs to broader demand-pull pressure looks mitigated.

Policy normalises further but does not get disruptive Related to inflation is how central banks respond and how that impacts growth.

Inflation upside had prompted some central banks in LATAM/CEEMEA to tighten significantly. The Fed’s taper is also underway. However, inflation dynamics in our space are markedly different than other EMs. Macrostability has also improved vs 2013. We see policy normalisation as the recovery firms, but aggressive hikes that short-circuit growth are unlikely.

相关报告

高盛中国市场策略-2022市场展望:“不适”的上行空间;离岸市场重回超配

5361

类型:策略

上传时间:2021-11

标签:投行报告、中国、市场展望)

语言:中文

金额:5积分

国际投行报告-全球芯片行业:芯片的冲突-台积电、三星和英特尔(英)

3978

类型:行研

上传时间:2022-06

标签:投行报告、芯片、冲突)

语言:英文

金额:5积分

HSBC-中国房地产和物业管理行业2022年展望-2021.11.9-75页

3506

类型:行研

上传时间:2021-11

标签:投行报告、房地产、物业)

语言:英文

金额:5积分

汇丰-中国汽车芯片

3128

类型:行研

上传时间:2022-07

标签:汽车、芯片、投行报告)

语言:英文

金额:5积分

HSBC-全球投资策略之未来城市:城市化形态的变化-2021.4-54页

2389

类型:策略

上传时间:2021-05

标签:投行报告、未来城市、城市化)

语言:英文

金额:5积分

瑞信-2021年全球财富报告(英)

2347

类型:专题

上传时间:2021-06

标签:全球财富、投行报告)

语言:英文

金额:5积分

2020东盟投资指南

2187

类型:专题

上传时间:2020-12

标签:东盟、投资指南)

语言:中文

金额:5积分

中国-东盟经贸合作:企业信心与展望调研报告

1788

类型:专题

上传时间:2021-09

标签:东盟、经贸、企业信心)

语言:中文

金额:5积分

瑞信-2022全球投资展望:股票、地区和宏观-2021.11.17-194页

1739

类型:宏观

上传时间:2021-11

标签:投行报告、2022投资展望、宏观经济)

语言:英文

金额:5积分

瑞信-全球财富报告2020-2020.10-56页

1553

类型:专题

上传时间:2020-10

标签:全球财富、投行报告)

语言:英文

金额:5积分

积分充值

30积分

6.00元

90积分

18.00元

150+8积分

30.00元

340+20积分

68.00元

640+50积分

128.00元

990+70积分

198.00元

1640+140积分

328.00元

微信支付

余额支付

积分充值

应付金额:

0 元

请登录,再发表你的看法

登录/注册