微信扫一扫联系客服

微信扫描二维码

进入报告厅H5

关注报告厅公众号

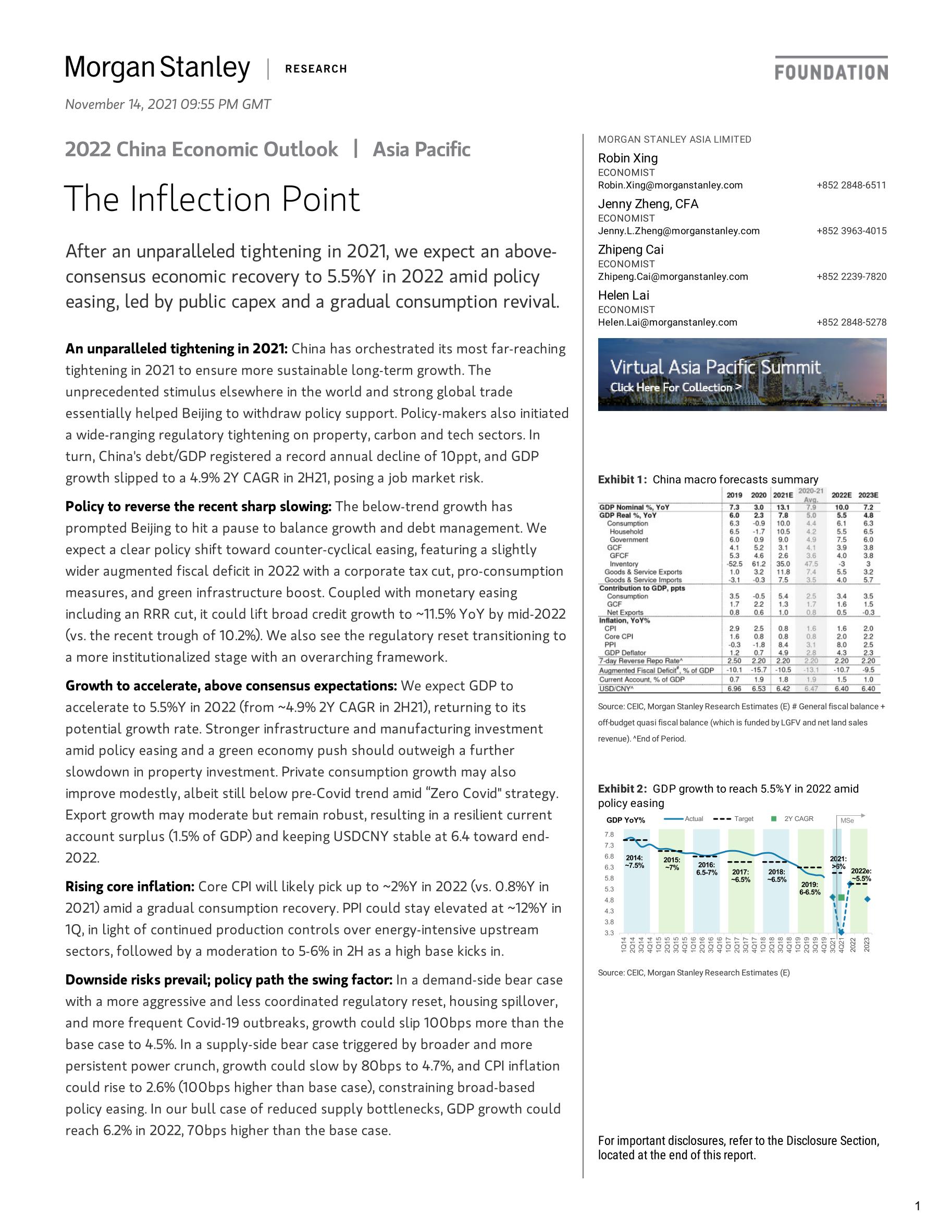

After an unparalleled tightening in 2021, we expect an aboveconsensus economic recovery to 5.5%Y in 2022 amid policy easing, led by public capex and a gradual consumption revival.

An unparalleled tightening in 2021: China has orchestrated its most far-reaching tightening in 2021 to ensure more sustainable long-term growth. The unprecedented stimulus elsewhere in the world and strong global trade essentially helped Beijing to withdraw policy support. Policy-makers also initiated a wide-ranging regulatory tightening on property, carbon and tech sectors. In turn, China's debt/GDP registered a record annual decline of 10ppt, and GDP growth slipped to a 4.9% 2Y CAGR in 2H21, posing a job market risk.

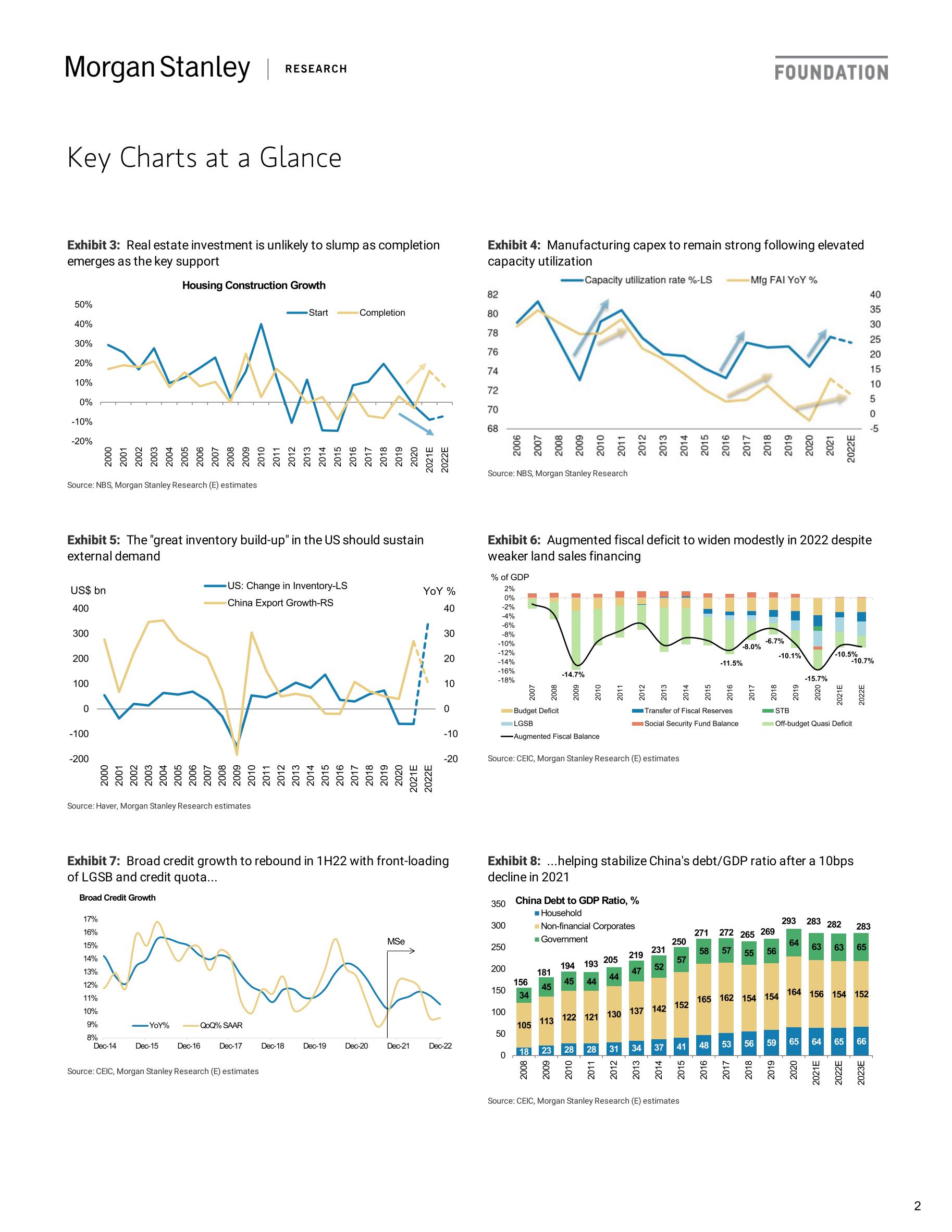

Policy to reverse the recent sharp slowing: The below-trend growth has prompted Beijing to hit a pause to balance growth and debt management. We expect a clear policy shift toward counter-cyclical easing, featuring a slightly wider augmented fiscal deficit in 2022 with a corporate tax cut, pro-consumption measures, and green infrastructure boost. Coupled with monetary easing including an RRR cut, it could lift broad credit growth to ~11.5% YoY by mid-2022 (vs. the recent trough of 10.2%). We also see the regulatory reset transitioning to a more institutionalized stage with an overarching framework.

Growth to accelerate, above consensus expectations: We expect GDP to accelerate to 5.5%Y in 2022 (from ~4.9% 2Y CAGR in 2H21), returning to its potential growth rate. Stronger infrastructure and manufacturing investment amid policy easing and a green economy push should outweigh a further slowdown in property investment. Private consumption growth may also improve modestly, albeit still below pre-Covid trend amid “Zero Covid" strategy.

Export growth may moderate but remain robust, resulting in a resilient current account surplus (1.5% of GDP) and keeping USDCNY stable at 6.4 toward end2022.

Rising core inflation: Core CPI will likely pick up to ~2%Y in 2022 (vs. 0.8%Y in 2021) amid a gradual consumption recovery. PPI could stay elevated at ~12%Y in 1Q, in light of continued production controls over energy-intensive upstream sectors, followed by a moderation to 5-6% in 2H as a high base kicks in.

Downside risks prevail; policy path the swing factor: In a demand-side bear case with a more aggressive and less coordinated regulatory reset, housing spillover, and more frequent Covid-19 outbreaks, growth could slip 100bps more than the base case to 4.5%. In a supply-side bear case triggered by broader and more persistent power crunch, growth could slow by 80bps to 4.7%, and CPI inflation could rise to 2.6% (100bps higher than base case), constraining broad-based policy easing. In our bull case of reduced supply bottlenecks, GDP growth could reach 6.2% in 2022, 70bps higher than the base case.

相关报告

高盛中国市场策略-2022市场展望:“不适”的上行空间;离岸市场重回超配

5354

类型:策略

上传时间:2021-11

标签:投行报告、中国、市场展望)

语言:中文

金额:5积分

国际投行报告-全球芯片行业:芯片的冲突-台积电、三星和英特尔(英)

3974

类型:行研

上传时间:2022-06

标签:投行报告、芯片、冲突)

语言:英文

金额:5积分

HSBC-中国房地产和物业管理行业2022年展望-2021.11.9-75页

3504

类型:行研

上传时间:2021-11

标签:投行报告、房地产、物业)

语言:英文

金额:5积分

汇丰-中国汽车芯片

3122

类型:行研

上传时间:2022-07

标签:汽车、芯片、投行报告)

语言:英文

金额:5积分

HSBC-全球投资策略之未来城市:城市化形态的变化-2021.4-54页

2382

类型:策略

上传时间:2021-05

标签:投行报告、未来城市、城市化)

语言:英文

金额:5积分

瑞信-2021年全球财富报告(英)

2345

类型:专题

上传时间:2021-06

标签:全球财富、投行报告)

语言:英文

金额:5积分

瑞信-2022全球投资展望:股票、地区和宏观-2021.11.17-194页

1737

类型:宏观

上传时间:2021-11

标签:投行报告、2022投资展望、宏观经济)

语言:英文

金额:5积分

瑞信-全球财富报告2020-2020.10-56页

1549

类型:专题

上传时间:2020-10

标签:全球财富、投行报告)

语言:英文

金额:5积分

瑞信-全球半导体行业:中国集成电路产业的不均衡崛起-2021.1.20-184页

1512

类型:行研

上传时间:2021-01

标签:半导体、中国集成电路、投行报告)

语言:英文

金额:5积分

瑞信-中国能源行业-中国氢能源:如何更好地发挥中国氢主题-2021.3.15-118页

1298

类型:行研

上传时间:2021-03

标签:能源、氢能源、投行报告)

语言:英文

金额:5积分

积分充值

30积分

6.00元

90积分

18.00元

150+8积分

30.00元

340+20积分

68.00元

640+50积分

128.00元

990+70积分

198.00元

1640+140积分

328.00元

微信支付

余额支付

积分充值

应付金额:

0 元

请登录,再发表你的看法

登录/注册