微信扫一扫联系客服

微信扫描二维码

进入报告厅H5

关注报告厅公众号

Shortfalls in private investment and human capital development as well as credit misallocation due to COVID-19 may slow potential growth by 0.6ppt over the next three years… …but gains from faster digitalisation should gradually offset the negative impact Policies such as reform and opening up also help to further minimise the medium-term shock to growth

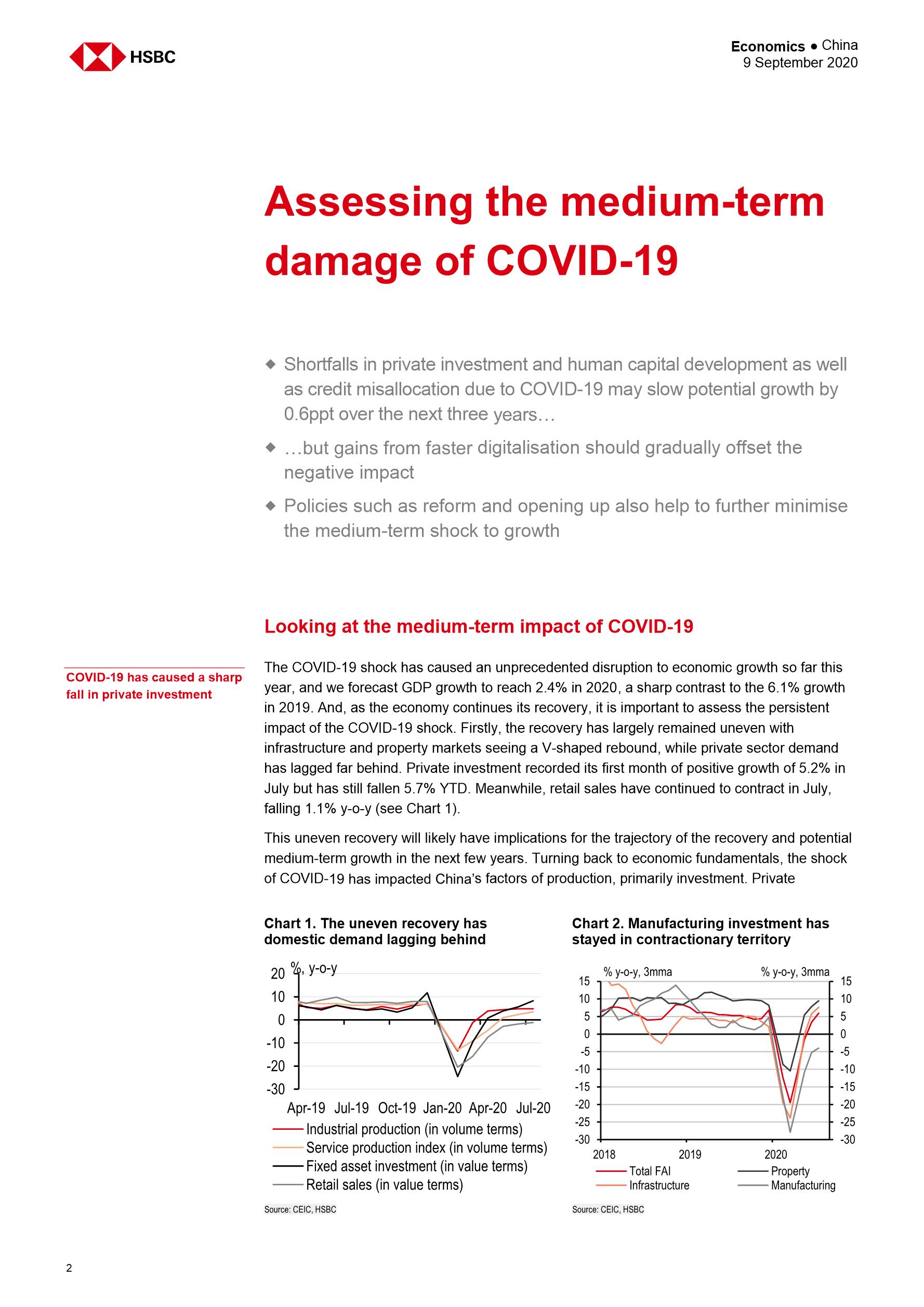

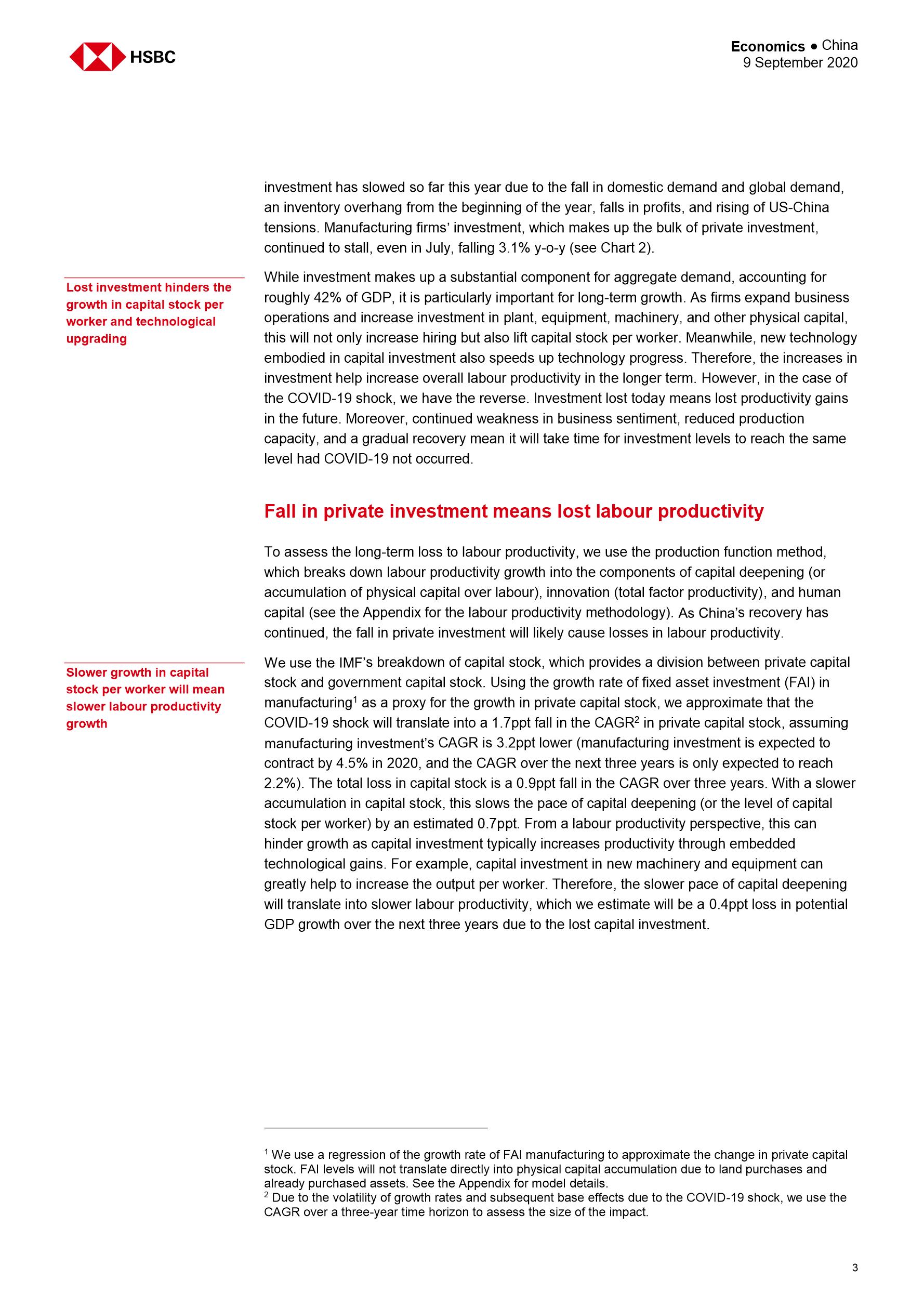

In this report, we look at the medium-term impact of COVID-19 on China’s labour productivity growth, which is likely to face a negative shock. Potential growth is expected to fall by roughly 0.6ppt on average over the next three years due to a slowdown in private investment, lost human capital gains, and credit misallocation. Private sector demand has lagged behind in the recovery, holding back private investment. In particular, after an unprecedented 12.7% y-o-y contraction in the first seven months, the recovery in private investment in manufacturing is likely to remain muted. This much weaker private investment means slower growth in capital stock per worker and, as such, labour productivity in the years ahead. Meanwhile, the COVID-19 crisis caused a large negative shock to labour markets, leading to the displacement of workers and delays in the career development for 8.7m fresh university graduates. Additionally, the pandemic has hit the private corporate sector harder than state-owned enterprises (SOEs). This has made state banks more reluctant to allocate credit to private firms, even though these firms are a more efficient user of credit, weighing on overall productivity growth.

That said, the COVID-19 shock has also spurred an acceleration in digitalisation and automation, helping partially offset the negative impact on productivity growth. Online retail sales of goods have jumped by 15.7% y-o-y YTD, while the domestic production of industrial robots has surged 10.4% y-o-y in H1. We expect this trend to continue in the coming years, helping to lift productivity growth. Moreover, Beijing’s infrastructurecentred stimulus package has led to a V-shaped recovery in infrastructure investment (including utilities) from a 16.5% y-o-y contraction in Q1 2020 to growth of over 9% in July. We expect infrastructure investment growth to accelerate to over 15% in coming quarters. In particular, what makes this round’s infrastructure push different is the focus on 5G and other ICT (e.g. AI, electrical vehicle infrastructure, and big data) basic facility building. This will likely foster innovation and, therefore, amplify the positive spill-over effect on productivity in the years ahead.

The implementation of structural reforms and opening up policy measures should also help to lessen the medium-term negative shocks and accelerate the rebound to prepandemic levels. In our view, further structural reforms and opening up are needed to help increase private sector confidence and boost private investment. Increased investment into human capital development, household registration reform, and measures to support job security can also help mitigate medium-term labour productivity losses.

This report replaces the version of the same date and title published earlier, to clarify the first bullet on the front page (it should refer to shortfalls in human capital development).

9

相关报告

高盛中国市场策略-2022市场展望:“不适”的上行空间;离岸市场重回超配

5357

类型:策略

上传时间:2021-11

标签:投行报告、中国、市场展望)

语言:中文

金额:5积分

国际投行报告-全球芯片行业:芯片的冲突-台积电、三星和英特尔(英)

3977

类型:行研

上传时间:2022-06

标签:投行报告、芯片、冲突)

语言:英文

金额:5积分

HSBC-中国房地产和物业管理行业2022年展望-2021.11.9-75页

3505

类型:行研

上传时间:2021-11

标签:投行报告、房地产、物业)

语言:英文

金额:5积分

汇丰-中国汽车芯片

3123

类型:行研

上传时间:2022-07

标签:汽车、芯片、投行报告)

语言:英文

金额:5积分

HSBC-全球投资策略之未来城市:城市化形态的变化-2021.4-54页

2387

类型:策略

上传时间:2021-05

标签:投行报告、未来城市、城市化)

语言:英文

金额:5积分

瑞信-2021年全球财富报告(英)

2346

类型:专题

上传时间:2021-06

标签:全球财富、投行报告)

语言:英文

金额:5积分

疫情影响下在华跨国企业不动产策略调研

1741

类型:专题

上传时间:2022-07

标签:疫情影响、跨国企业、不动产)

语言:中文

金额:5积分

瑞信-2022全球投资展望:股票、地区和宏观-2021.11.17-194页

1738

类型:宏观

上传时间:2021-11

标签:投行报告、2022投资展望、宏观经济)

语言:英文

金额:5积分

瑞信-全球财富报告2020-2020.10-56页

1551

类型:专题

上传时间:2020-10

标签:全球财富、投行报告)

语言:英文

金额:5积分

瑞信-全球半导体行业:中国集成电路产业的不均衡崛起-2021.1.20-184页

1515

类型:行研

上传时间:2021-01

标签:半导体、中国集成电路、投行报告)

语言:英文

金额:5积分

积分充值

30积分

6.00元

90积分

18.00元

150+8积分

30.00元

340+20积分

68.00元

640+50积分

128.00元

990+70积分

198.00元

1640+140积分

328.00元

微信支付

余额支付

积分充值

应付金额:

0 元

请登录,再发表你的看法

登录/注册