微信扫一扫联系客服

微信扫描二维码

进入报告厅H5

关注报告厅公众号

Sector has appreciated on strong policy expectations; in this report, we answer some of the key questions from investors

On an enhanced industry outlook, TPs are lifted with more bullish assumptions; next catalysts and risks are highlighted

Stocks: Buys on Xinyi Solar (glass), Tongwei (poly), Xinyi Energy (farm); upgrade GCL (poly) to Hold (from Reduce)

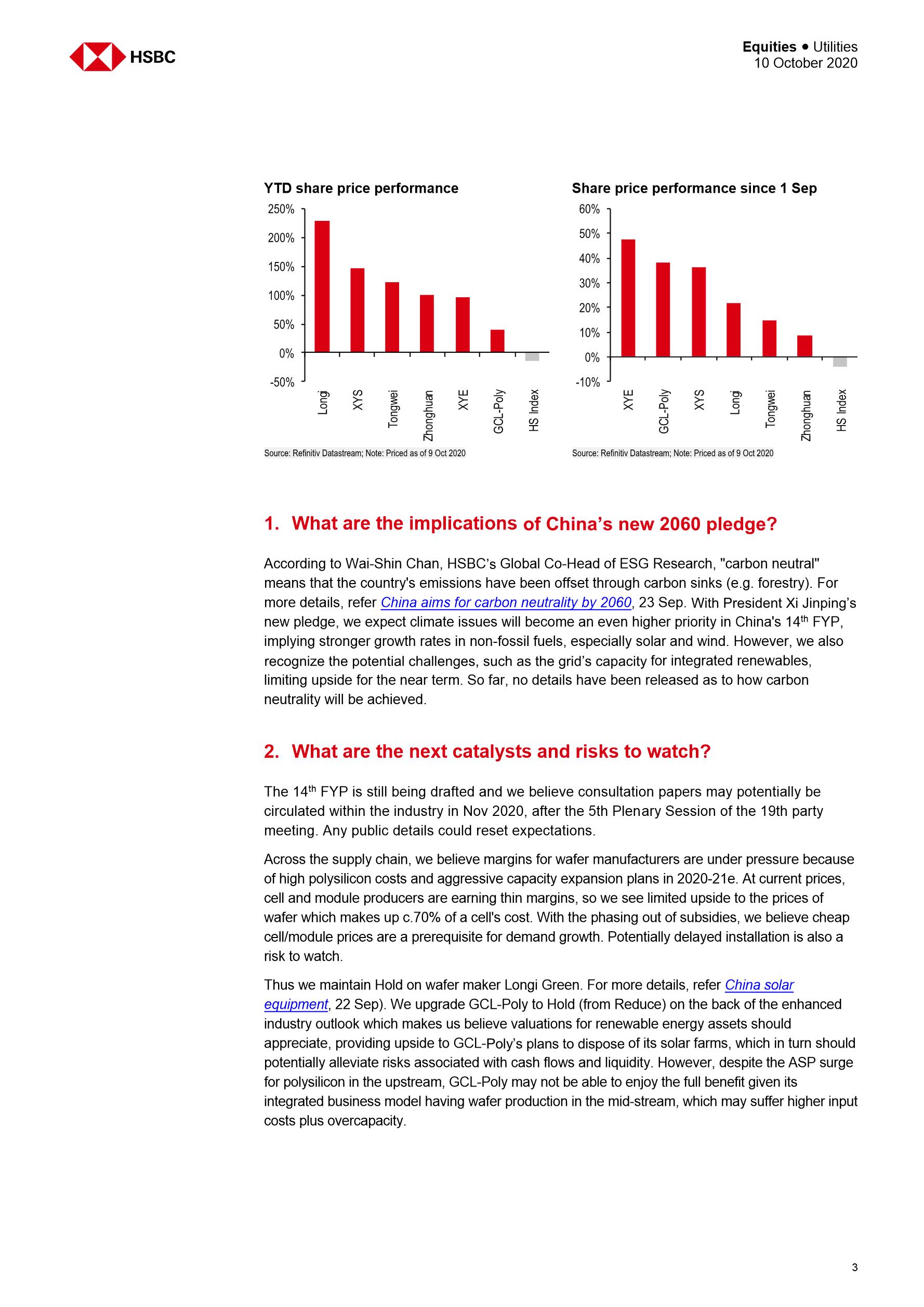

Understanding this solar boom: The recent surge in solar stocks, in our view, could be explained by 1) recent news (bjx, 14 Sep) on some bullish targets for the upcoming 14th Five Year Plan (FYP) by 2025, such as a combined installation for solar and wind of c.100GW p.a. (2016-19: 54-68GW p.a.), and 2) President Xi Jinping’s recent target to achieve carbon neutrality by 2060. While these bode well for solar energy over the long term, we stay selective across the supply chain in terms of subsets/stocks. This report highlights our answers to some key investor questions:

1. What are the implications of China’s new 2060 pledge? We expect climate issues will become an even higher priority in China's 14th FYP, implying stronger growth rates in non-fossil fuels, especially solar and wind. However, we also recognize the potential challenges, such as the grid’s capacity for integrated renewables, limiting upside for the near term. So far, no details have been released as to how carbon neutrality will be achieved (see China's new climate ambition, 29 Sep).

2. What are the next catalysts and risks to watch? The 14th FYP is still being drafted and we believe consultation papers may potentially be circulated within the industry in Nov 2020, after the 5th Plenary Session of the 19th party meeting. Any public details could reset expectations. We continue to see risks in solar wafers because of high input costs and overcapacity in 2020-21 (see Polysilicon price hikes could squeeze wafer margins, 23 Sep).

3. Will recent price hikes in solar products discourage demand? Given supply tightness, module prices have risen 1-6% since July. We believe certain installations may be delayed into 2021 as operators are hoping module prices will retreat after the current spike. We maintain our 40GW installation in China for 2020, versus the market’s more optimistic 45GW (see Reassessing the demand curve, 23 Sep).

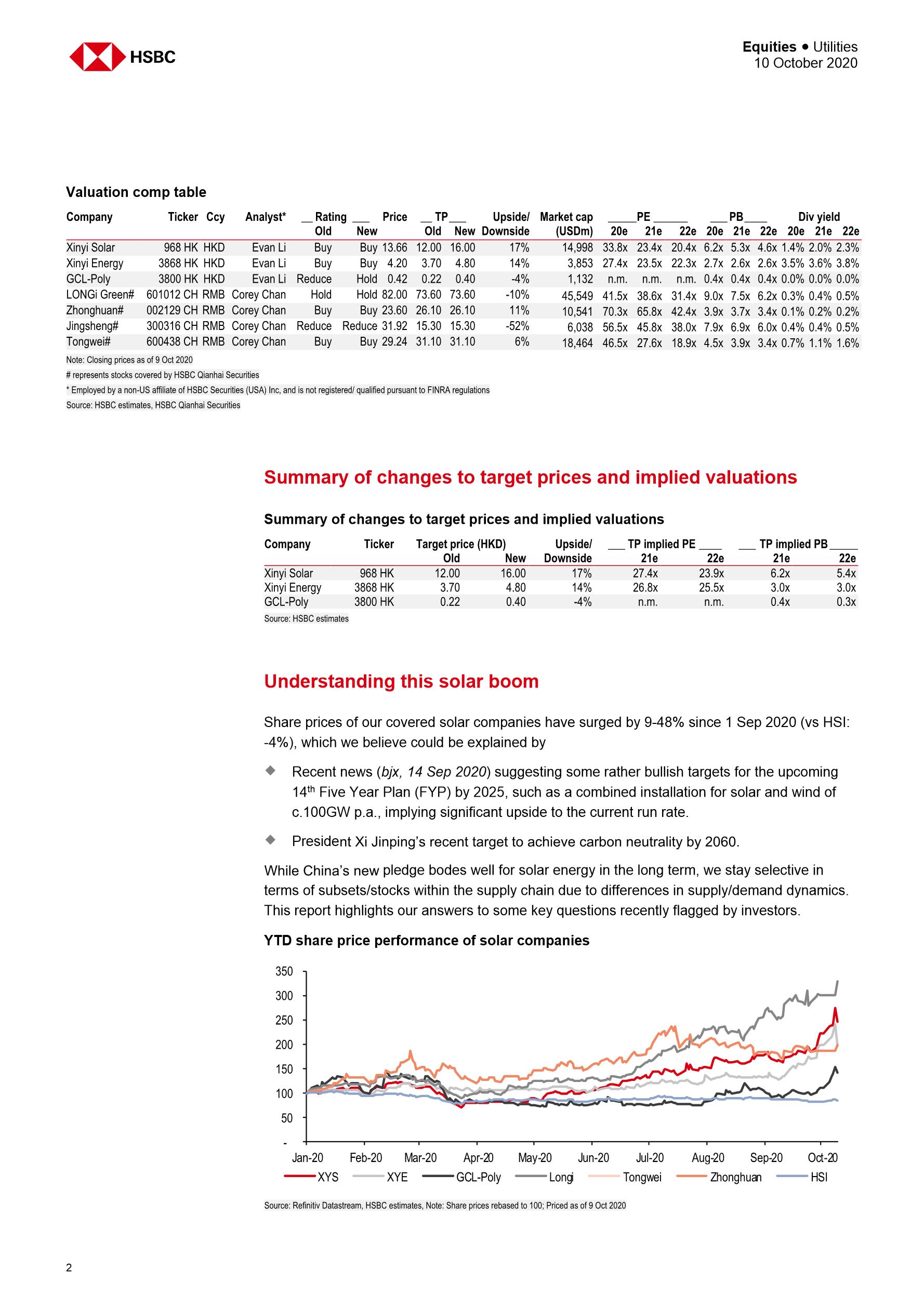

4. Stocks: Moving into bullish scenarios? We continue to favour polysilicon, solar glass and solar farms. For major solar glass maker Xinyi Solar (XYS, 968 HK), we lift TP to HKD16 (from HKD12) because of more bullish assumptions in the medium-term where our shipment numbers imply a national market of 60-85GW p.a. during 2023-25 (global: 168-127GW) based on the same market share, vs our current house view of 40-47GW p.a. for 2020-22. Similarly, we raise TP for solar farm operator Xinyi Energy (XYE, 3868 HK) to HKD4.8 (from HKD3.7) by assuming more capacity additions. We upgrade GCL Poly to Hold (from Reduce) and lift TP to HKD0.40 (from HKD0.22) based on a better shipment outlook, despite its liquidity risks.

相关报告

高盛中国市场策略-2022市场展望:“不适”的上行空间;离岸市场重回超配

5356

类型:策略

上传时间:2021-11

标签:投行报告、中国、市场展望)

语言:中文

金额:5积分

国际投行报告-全球芯片行业:芯片的冲突-台积电、三星和英特尔(英)

3975

类型:行研

上传时间:2022-06

标签:投行报告、芯片、冲突)

语言:英文

金额:5积分

光伏产业链全景图

3609

类型:行研

上传时间:2022-09

标签:光伏、太阳能)

语言:中文

金额:免费

HSBC-中国房地产和物业管理行业2022年展望-2021.11.9-75页

3504

类型:行研

上传时间:2021-11

标签:投行报告、房地产、物业)

语言:英文

金额:5积分

汇丰-中国汽车芯片

3123

类型:行研

上传时间:2022-07

标签:汽车、芯片、投行报告)

语言:英文

金额:5积分

HSBC-全球投资策略之未来城市:城市化形态的变化-2021.4-54页

2386

类型:策略

上传时间:2021-05

标签:投行报告、未来城市、城市化)

语言:英文

金额:5积分

瑞信-2021年全球财富报告(英)

2346

类型:专题

上传时间:2021-06

标签:全球财富、投行报告)

语言:英文

金额:5积分

瑞信-2022全球投资展望:股票、地区和宏观-2021.11.17-194页

1738

类型:宏观

上传时间:2021-11

标签:投行报告、2022投资展望、宏观经济)

语言:英文

金额:5积分

瑞信-全球财富报告2020-2020.10-56页

1550

类型:专题

上传时间:2020-10

标签:全球财富、投行报告)

语言:英文

金额:5积分

瑞信-全球半导体行业:中国集成电路产业的不均衡崛起-2021.1.20-184页

1512

类型:行研

上传时间:2021-01

标签:半导体、中国集成电路、投行报告)

语言:英文

金额:5积分

积分充值

30积分

6.00元

90积分

18.00元

150+8积分

30.00元

340+20积分

68.00元

640+50积分

128.00元

990+70积分

198.00元

1640+140积分

328.00元

微信支付

余额支付

积分充值

应付金额:

0 元

请登录,再发表你的看法

登录/注册