微信扫一扫联系客服

微信扫描二维码

进入报告厅H5

关注报告厅公众号

In broad terms, accounting standards aim to enable employers to approximate the cost of an employee’s pension or other postretirement benefit over that employee’s service tenure. Any benefit accounting method that recognizes the cost of benefits before their payment becomes due must be based on estimates or assumptions about future events that will determine the amount and timing of benefit payments.

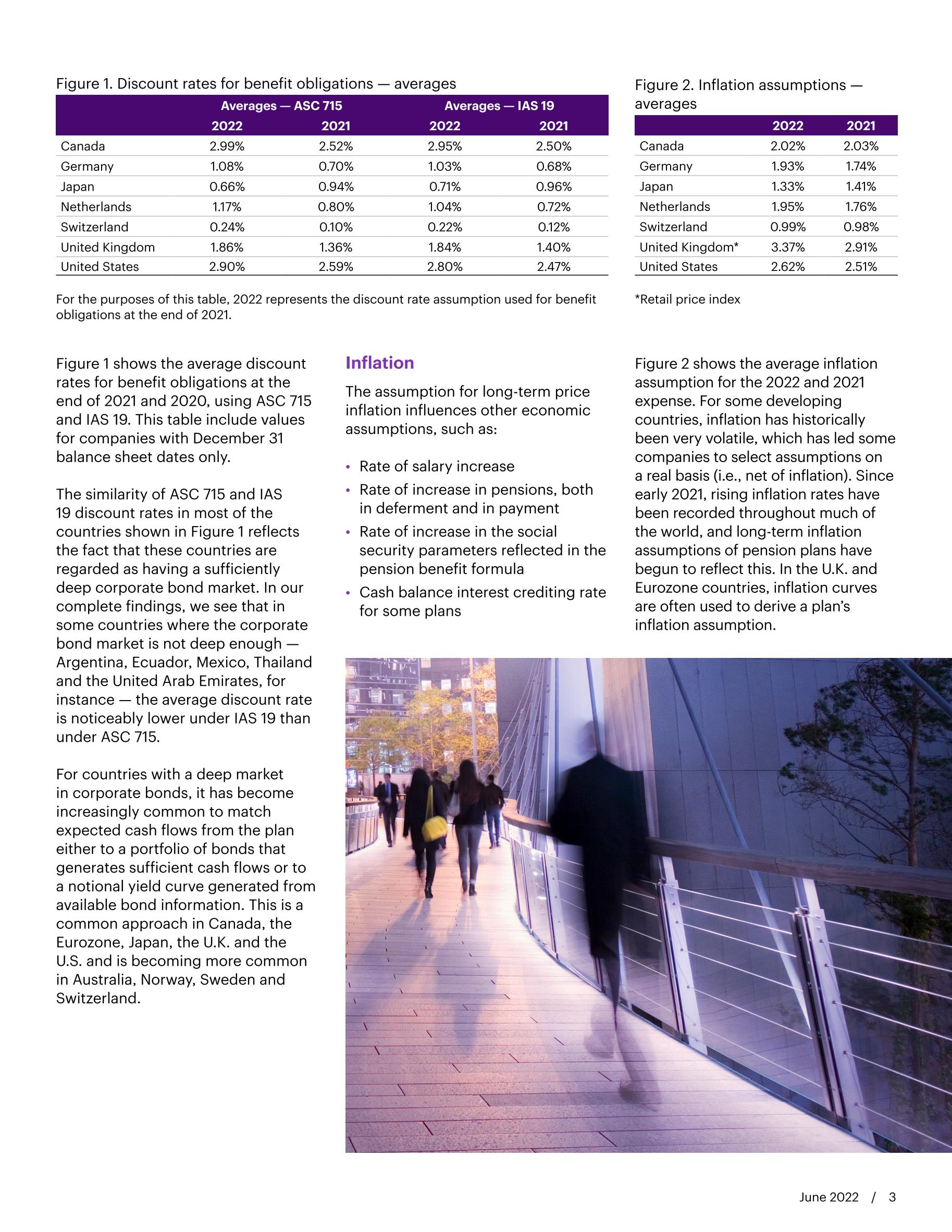

Two key economic assumptions in the determination of benefit costs under an accounting standard are the discount rate and inflation.

Under ASC 715, there is another key economic assumption: the expected long-term rate of return on plan assets (for funded plans). In many countries, four additional economic assumptions, which are somewhat linked to inflation, can play a key role: (1) rate of salary increase; (2) rate of increase in pensions, both in deferment and in payment; (3) cash balance interest crediting rate; and (4) rate of increase in the social security parameters reflected in the pension benefit formula. We discuss these in our full report.

Although this survey mainly explores economic assumptions, we have again shown data regarding mortality assumptions, which are receiving closer attention because of increasing longevity.

相关报告

固定收益专题报告:城投与土地-20211102-中泰证券-38页

815

类型:策略

上传时间:2021-11

标签:固定收益、城投、土地)

语言:中文

金额:免费

固定收益专题:31省、383地市、689区县债务率全测算,谁的债高?-20210112-国盛证券-25页

761

类型:专题

上传时间:2021-01

标签:固定收益、债务)

语言:中文

金额:免费

HSBC-全球固定收益资产配置-2020.7.7-33页

726

类型:专题

上传时间:2020-07

标签:固定收益、资产配置、投行报告)

语言:英文

金额:5积分

固定收益专题报告:融资租赁行业与债券深度梳理-20200813-国金证券-34页

639

类型:专题

上传时间:2020-08

标签:固定收益、融资租赁、债券)

语言:中文

金额:免费

德银-全球投资策略之全球固定收益2021年展望:还需要迎头赶上-2020.12.22-110页

628

类型:策略

上传时间:2021-01

标签:投资策略、固定收益)

语言:英文

金额:5积分

固定收益专题:地产债基本面系列之二,房企违约案例全复盘-20210401-国盛证券-75页

612

类型:行研

上传时间:2021-04

标签:固定收益、地产债、房企违约案例)

语言:中文

金额:免费

电子书-固定收益证券手册(英)

610

类型:电子书

上传时间:2021-07

标签:定量投资、固定收益、政权)

语言:英文

金额:5积分

固定收益专题:一文览尽融资担保行业-20210923-国盛证券-40页

582

类型:专题

上传时间:2021-09

标签:固定收益、融资担保)

语言:中文

金额:免费

固定收益2021年投资策略:债牛回归-20201117-中信证券-40页

514

类型:策略

上传时间:2020-11

标签:固定收益、投资策略)

语言:中文

金额:免费

J.P. 摩根-全球投资策略之全球固定收益市场展望2021-2020.11.27-135页

508

类型:策略

上传时间:2020-12

标签:全球投资策略、固定收益、投行报告)

语言:英文

金额:5积分

积分充值

30积分

6.00元

90积分

18.00元

150+8积分

30.00元

340+20积分

68.00元

640+50积分

128.00元

990+70积分

198.00元

1640+140积分

328.00元

微信支付

余额支付

积分充值

应付金额:

0 元

请登录,再发表你的看法

登录/注册