微信扫一扫联系客服

微信扫描二维码

进入报告厅H5

关注报告厅公众号

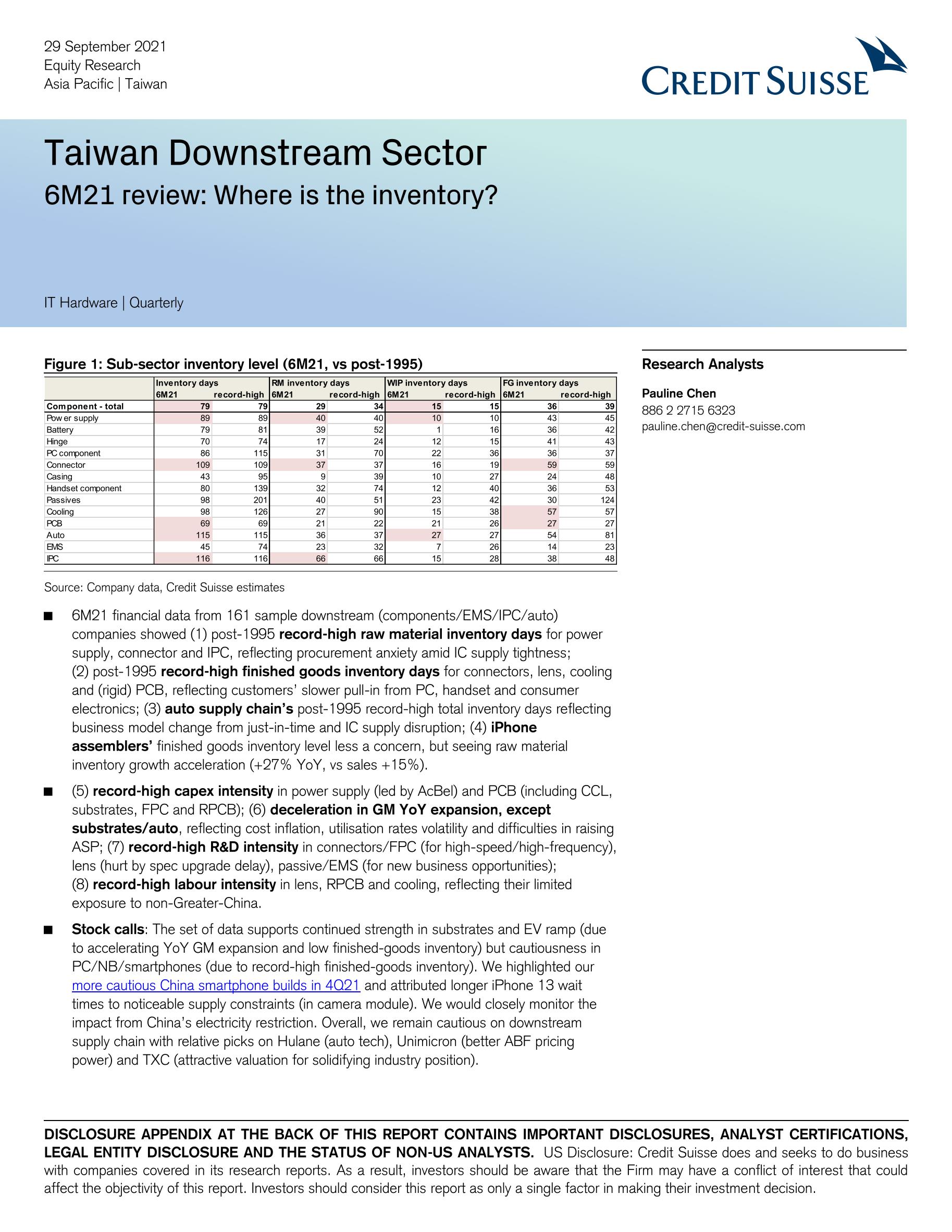

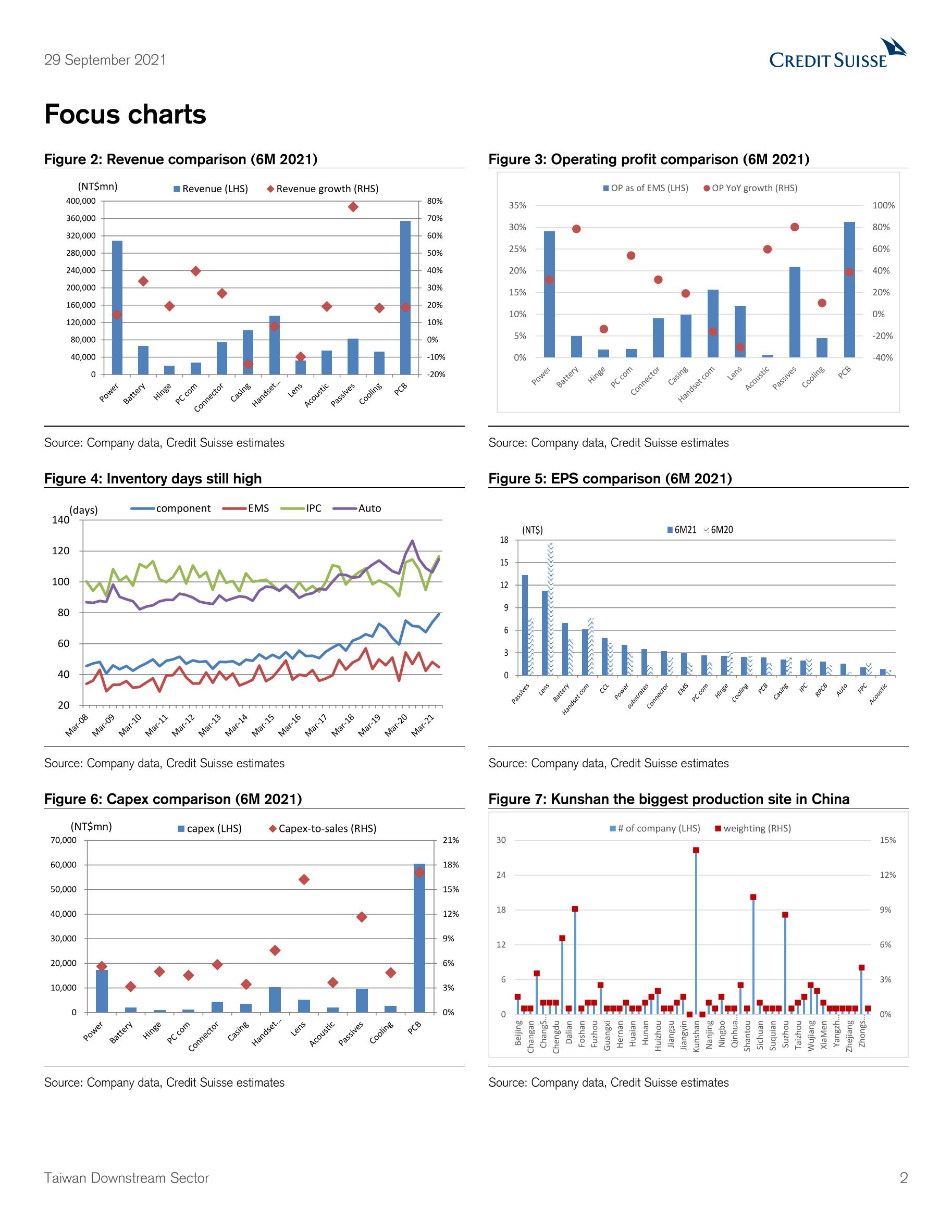

6M21 financial data from 161 sample downstream (components/EMS/IPC/auto) companies showed (1) post-1995 record-high raw material inventory days for power supply, connector and IPC, reflecting procurement anxiety amid IC supply tightness; (2) post-1995 record-high finished goods inventory days for connectors, lens, cooling and (rigid) PCB, reflecting customers’ slower pull-in from PC, handset and consumer electronics; (3) auto supply chain’s post-1995 record-high total inventory days reflecting business model change from just-in-time and IC supply disruption; (4) iPhone assemblers’ finished goods inventory level less a concern, but seeing raw material inventory growth acceleration (+27% YoY, vs sales +15%).

(5) record-high capex intensity in power supply (led by AcBel) and PCB (including CCL, substrates, FPC and RPCB); (6) deceleration in GM YoY expansion, except substrates/auto, reflecting cost inflation, utilisation rates volatility and difficulties in raising ASP; (7) record-high R&D intensity in connectors/FPC (for high-speed/high-frequency), lens (hurt by spec upgrade delay), passive/EMS (for new business opportunities); (8) record-high labour intensity in lens, RPCB and cooling, reflecting their limited exposure to non-Greater-China.

Stock calls: The set of data supports continued strength in substrates and EV ramp (due to accelerating YoY GM expansion and low finished-goods inventory) but cautiousness in PC/NB/smartphones (due to record-high finished-goods inventory). We highlighted our more cautious China smartphone builds in 4Q21 and attributed longer iPhone 13 wait times to noticeable supply constraints (in camera module). We would closely monitor the impact from China’s electricity restriction. Overall, we remain cautious on downstream supply chain with relative picks on Hulane (auto tech), Unimicron (better ABF pricing power) and TXC (attractive valuation for solidifying industry position).

相关报告

高盛中国市场策略-2022市场展望:“不适”的上行空间;离岸市场重回超配

5362

类型:策略

上传时间:2021-11

标签:投行报告、中国、市场展望)

语言:中文

金额:5积分

国际投行报告-全球芯片行业:芯片的冲突-台积电、三星和英特尔(英)

3979

类型:行研

上传时间:2022-06

标签:投行报告、芯片、冲突)

语言:英文

金额:5积分

HSBC-中国房地产和物业管理行业2022年展望-2021.11.9-75页

3507

类型:行研

上传时间:2021-11

标签:投行报告、房地产、物业)

语言:英文

金额:5积分

汇丰-中国汽车芯片

3131

类型:行研

上传时间:2022-07

标签:汽车、芯片、投行报告)

语言:英文

金额:5积分

HSBC-全球投资策略之未来城市:城市化形态的变化-2021.4-54页

2390

类型:策略

上传时间:2021-05

标签:投行报告、未来城市、城市化)

语言:英文

金额:5积分

瑞信-2021年全球财富报告(英)

2347

类型:专题

上传时间:2021-06

标签:全球财富、投行报告)

语言:英文

金额:5积分

瑞信-2022全球投资展望:股票、地区和宏观-2021.11.17-194页

1740

类型:宏观

上传时间:2021-11

标签:投行报告、2022投资展望、宏观经济)

语言:英文

金额:5积分

瑞信-全球财富报告2020-2020.10-56页

1553

类型:专题

上传时间:2020-10

标签:全球财富、投行报告)

语言:英文

金额:5积分

瑞信-全球半导体行业:中国集成电路产业的不均衡崛起-2021.1.20-184页

1515

类型:行研

上传时间:2021-01

标签:半导体、中国集成电路、投行报告)

语言:英文

金额:5积分

瑞信-中国能源行业-中国氢能源:如何更好地发挥中国氢主题-2021.3.15-118页

1302

类型:行研

上传时间:2021-03

标签:能源、氢能源、投行报告)

语言:英文

金额:5积分

积分充值

30积分

6.00元

90积分

18.00元

150+8积分

30.00元

340+20积分

68.00元

640+50积分

128.00元

990+70积分

198.00元

1640+140积分

328.00元

微信支付

余额支付

积分充值

应付金额:

0 元

请登录,再发表你的看法

登录/注册